This article is part of the Under the Lens series

The Racial Wealth Gap—Moving to Systemic Solutions

Never Scared, Rock dives head first into the ever-growing racial wealth gap, proclaiming that ”there are no wealthy Black or brown people in America. We got some rich ones, [but] we don’t got no f***ing wealth. Shaq is rich; the white man who signs his check is wealthy.”

Sadly, he’s right, and his joke is supported by volumes of research documenting that the racial wealth gap has grown exponentially over time. If nothing is done, people of color will be permanently excluded from the middle class. According to a report by the Institute for Policy Studies: “If average Black family wealth continues to grow at the same pace it has over the past three decades, it would take Black families 228 years to amass the same amount of wealth White families have today. That’s just 17 years shorter than the 245-year span of slavery in this country.”

In recent years, it’s become increasingly popular to address the racial wealth gap. Everyone—from policy advocates, and government officials, to nonprofit organizations, and corporate responsibility officers—claims to have the answers. Though many are acting in good faith, most of the solutions offered are rooted in wealth-building initiatives, predominantly focused on increasing homeownership, business ownership, and the personal savings of Black people.

During his campaign and throughout his term so far, President Joe Biden has committed to addressing “the issue of racial equity,” mainstreaming many of those same wealth-building ideas to fix the racial wealth gap. Even major corporations, including JPMorganChase, Bank of America, and Wells Fargo, have pledged to throw millions of dollars at closing the racial wealth gap.

While these wealth-building initiatives are laudable, most of them will fail because they do not address the root cause of the racial wealth gap: wealth extraction.

The racial wealth gap is a systemic problem, not a product of Black people’s personal choices. And no matter how many wealth-building opportunities we create for Black people and other people of color, these efforts will never deliver if we leave the wealth-stripping processes intact.

Unfortunately, racism is profitable. We are living in what my organization has termed an “Oppression Economy,” in which predominantly white policymakers and white-led corporations and academic institutions wield economic and political power over the systems that determine the lives and livelihoods of Black and brown people.

Exclusion, exploitation, and extraction uphold both economic oppression and the wealth of elite white people. The exclusion of people of color denies them access to the essential financial products and services necessary to navigate our economy, such as banking and credit accounts. Exploitation is the intentional use of the country’s racial caste system to normalize and deeply embed racist financial structures and double standards in our economy (e.g., the reliance on credit scoring). Finally, the wealthy elite use the resulting insecurity that people of color experience as a tool of extraction to steal their income and wealth through predatory financial products and services. The Oppression Economy and the people in power who sustain it intentionally target Black people and other non-Black people of color. The system is built to financially prey upon Black people, which contributes, by design, to criminalizing and politically silencing them. The priority is always corporate profits over Black lives, profits and wealth they could not obtain if racism were not profitable.

wealth extraction in a dual financial system

The financial services industry is central to the Oppression Economy. This industry, which includes banks, asset management companies, insurance companies, and private equity companies, controls the flow of money in our economy. Through an elaborate network of financial products, services, and instruments this system is built for extraction—removing capital from precisely the people who have the least to start with. We refer to it as a “dual financial system” because it delivers very different sets of products—and results—for wealthy white people and for people of color.

Black people and other people of color are by design excluded from accessing the very products and services that provide households with financial security. This includes bank accounts, retirement and personal savings accounts, prime credit cards, insurance, mortgages, and small business loans. They may be excluded by geography (lack of bank branches, or higher auto insurance rates in formerly redlined neighborhoods), lower wages due to employment discrimination and segregation, the wealth gap itself (for example, account minimums, or lack of a cushion to maintain on-time payments during an emergency), or outright lending bias.

This exclusion then leads to a vicious cycle: the financial services industry exploits the very insecurity it has created by offering predatory products and services, which strip income and wealth, to Black people and other communities of color who have been kept from access to better ones.

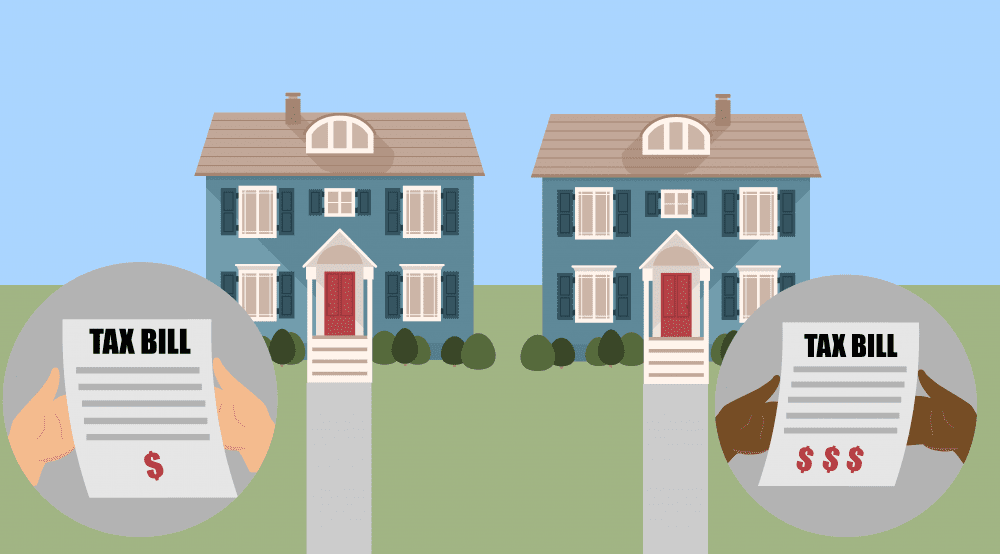

People of color who need to close holes in monthly cash flow because of low wages, lack of an asset cushion, inconsistent cash flow, and stripped wealth are forced to take out payday loans that charge interest rates of up to 700 percent. Black people also receive fewer discounts and more penalties when purchasing auto insurance, which means we pay significantly more than white households. Additionally, when we can access mortgage credit to purchase a home, we are more likely to receive mortgage products with adjustable (and often escalating) interest rates or are just straight up confronted with higher fixed interest rates than rates enjoyed by white households. This extraction isn’t happening simply because financial actors don’t like Black and brown people. It’s because there’s a lot of profit to be gained from desperation.

This dual system is amplified by the credit reporting system, because all of the consequences to racial financial exclusion also lead to lower credit scores, which are in turn used to further exclusion. Three credit reporting megacorporations—Experian, TransUnion, and Equifax—act as financial overseers that determine who can and cannot access wealth-building financial products, services, and capital.

Though it is illegal to use race to determine access to financial services, the credit score produced by these agencies has become a proxy for racial discrimination. It’s outright baked into these scores by their reliance on measures that have a long history of bias. For example, the on-time bill payment measure favors mortgage and credit card payments (which many Black people are excluded from accessing) over rental and cell phone payments (which more Black people have greater access to). Debt types that are more likely to be held by Black people (e.g., payday or student loans) are treated negatively, compounding the impact of financial exclusion.

Those with high credit scores can build wealth through affordable mortgages, prime lines of credit, and low-cost credit cards. Those who do not have high credit scores have wealth stripped away because they cannot access affordable credit. Without affordable credit they either take on more expensive or possibly predatory credit, or go without things that typically require credit to purchase—such as a car that won’t break down regularly or home repairs. Doing without these things also tends to cost more in the long run and makes building wealth difficult.

As I testified before Congress, the credit-scoring system reinforces and exacerbates racial inequities. Black people and other non-Black communities pay more for basic financial services than white people do, and ultimately experience wealth-stripping because of it.

Other methods of extracting wealth happen in the public safety and health care sectors. Overpolicing in Black communities and mass incarceration extract wealth through excessive fines and fees, including child support debt to the state that accumulates during incarceration. A racist health care system, refusal of some states to expand Medicaid, and the toll of living in a white supremacist society all lead to worse health care outcomes for Black people and also extract wealth, in the form of excess medical debt.

This racist process of exclusion and extraction is driven by the financial industry’s thirst for profits and wealth, and it’s made possible by the broader existence of our nation’s racial caste system.

These systems of exclusion and extraction make it much harder for Black households to benefit from the wealth-building strategies typically recommended. For example, Black homeowners experience widespread appraisal discrimination, resulting in lower valuations of their homes and less home equity, and as a result, lower wealth than white homeowners. Black businesses are frequently undervalued as compared to white-owned businesses, thus lowering the overall wealth of Black business owners. The inability of Black people and other people of color to build wealth as a result of this systemic racism forces homeowners, business owners, and households of color more broadly to rely on predatory debt just to survive.

Many forms of wealth extraction occur every day in America. The Oppression Economy has been with us since the nation’s founding and is deeply embedded in our economic systems, as seen in our credit system and labor market. Like any thriving ecosystem, the Oppression Economy constantly evolves, thwarting our individual efforts to overcome oppression and build wealth.

Proposals to build wealth for people of color, especially Black people, are important, necessary even. But until we dismantle the many systems of wealth extraction and the power structures that support them, the racial wealth gap will remain.

Thanks for giving me a new framework for thinking about the wealth gap: exclusion, exploitation, and extraction, Jeremie. While reform of the dominant financial/ownership system is clearly needed, I’d be interested in hearing what you think about black-owned/led agricultural cooperatives and worker-owned businesses.

Yes, thank you, Mr. Greer. This framework is very compelling and so well presented and argued here. I look forward to using and sharing with others. I so appreciate it.

There are a lot of whites who are not wealthy, and a fair number who face most of the injustices you describe.

All this is true, but is not talked about politically. And as Howard notes, racial division is just one of many mechanisms that facilitates the economy based on extraction from some for the benefit of others. This makes it harder to do anything about because it is so easy to divide people over personal interactions, personal hurts and disrespects ,and social identity. Since finance capital is so mobile compared to human beings, it would be good if there was a consensus that finance should be a something like public utility, which serves the productive economy rather than the other way around. And thee need to be institutions that spread social capital and decision making power, rather than concentrating them.