A: Yes!

A: Yes!

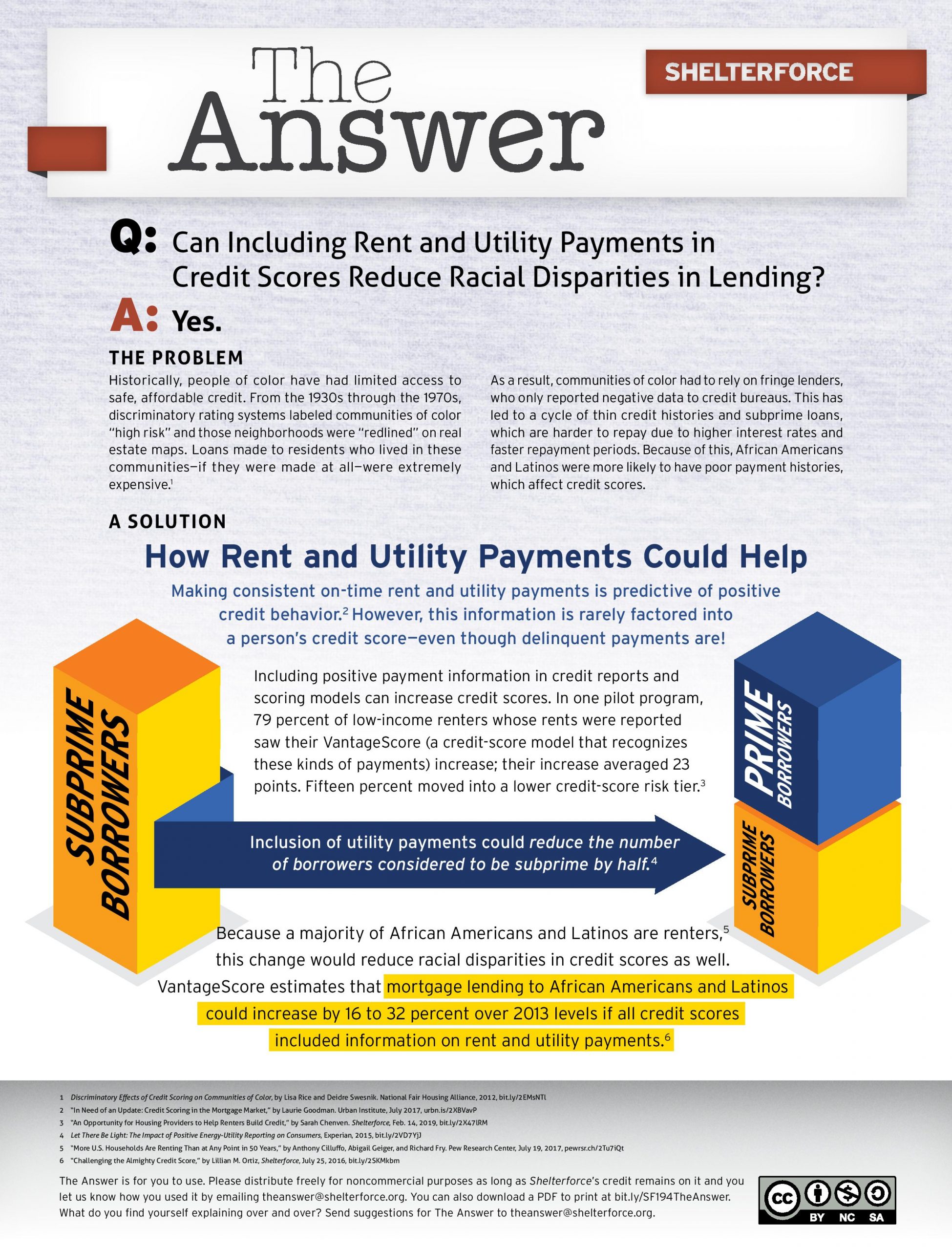

Historically, people of color have had limited access to safe, affordable credit. From the 1930s through the 1970s, discriminatory rating systems labeled communities of color “high risk” and those neighborhoods were “redlined” on real estate maps. Loans made to residents who lived in these communities—if they were made at all—were extremely expensive. As a result, communities of color had to rely on fringe lenders, who only reported negative data to credit bureaus. This has led to a cycle of thin credit histories and subprime loans, which are harder to repay due to higher interest rates and faster repayment periods. Because of this, African Americans and Latinos were more likely to have poor payment histories, which affect credit scores. Making consistent on-time rent and utility payments is predictive of positive credit behavior. However, this information is rarely factored into a person’s credit score by the models—even though delinquent payments are! Including positive payment information in credit reports and scoring models can increase credit scores. In one pilot program, 79 percent of low-income renters whose rents were reported saw their VantageScore (a credit-score model that recognizes these kinds of payments) increase, and that increase averaged 23 points. Fifteen percent moved into a lower credit-score risk tier. Inclusion of utility payments could reduce the number of borrowers considered to be subprime by half. Because a majority of African Americans and Latinos are renters, this change could reduce racial disparities in credit scores as well. VantageScore estimates that mortgage lending to African Americans and Latinos could increase by 16 to 32 percent over 2013 levels if all credit scores included information on rent and utility payments. The Problem

How Rent and Utility Payments Could Help

The Answer is for you to use. Please distribute freely for noncommercial purposes as long as Shelterforce’s credit remains on it and you let us know how you used it by emailing [email protected].

What do you find yourself explaining over and over? Send suggestions for The Answer to [email protected].About the Author

![]()

Tags

Comments

2 thoughts on “Q: Can Including Rent and Utility Payments in Credit Scores Reduce Racial Disparities in Lending?”

Leave a Reply

Having a hard time with this as credit score is not predictive of renters’ ability To pay rents but also tends to be the same barriers Renter’s face when trying to secure rental housing (higher security deposits, out-right denials). This is problematic because in some instances people’s credit went bad when they had to prioritize rent payment over credit card scores, etc. Including rental payments and utility payments in credit scores could inadvertently create higher barriers for Black and Latino Renters who often move more frequently than their counterparts.

Katrina, could you explain what you mean about credit scores not being predictive of renters’ ability to make rental payments? I completely agree about credit scores being a pressing obstacle for many trying to secure affordable rental housing, but is one’s credit score not, at least in significant part, a reflection of the individual’s historic ability to pay for expenses they incurred?

I understand how prioritizing rent payments over credit card bills might hurt individuals by forcing them to accept interest fees on unpaid credit expenses for the sake of meeting monthly rents, but this dichotomy seems more a failure on the part of state legislators to protect constituents against predatory consumer and lending practices. Although, failing to pay a credit debt in full doesn’t alone hurt an individual’s credit score unless that failure becomes repetitive and systemic at which point way bigger issues than a credit score come into the picture.

Don’t you think that if rental and utility payments were included in credit scores barriers would lower as renters move, demonstrating a consistency of making payments on both over time? I’m interested in your thoughts on this.