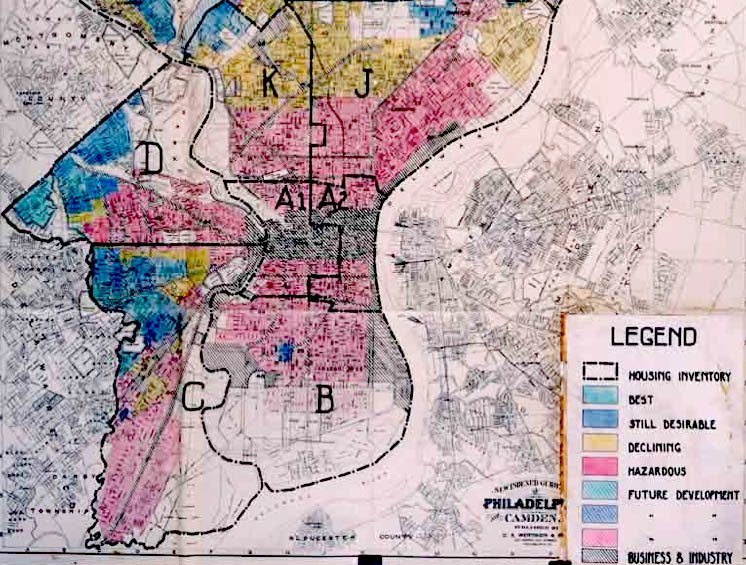

A Homeowners Loan Corporation redlining map from the 1930s. The OCC and FDIC CRA reform proposal could bring us back here.

Legalized redlining. That would be the result if a currently proposed rule to “modernize” the Community Reinvestment Act (CRA) is adopted by the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC).

And it breaks my heart.

There is a lot to dislike about the proposed rule. First, it dramatically and irresponsibly expands what activities would be eligible for CRA credit. The proposed “non-exhaustive list” of eligible activities now includes infrastructure, transportation, and even sports stadiums. Eligible activities would no longer be required to primarily benefit low- and moderate-income communities.

Second, the proposed rule shifts the way financial institutions are assessed on the goal of appropriately serving all communities where they do business to a single ratio: CRA-eligible dollars invested ÷ deposits = CRA rating

This single-ratio approach completely disregards whether the community development and financial needs of the community are being served by the bank or its investments. And as a result, the community development organizations that have served marginalized neighborhoods for years, even decades, and whose experience and expertise is seriously considered as part of the CRA examination process, will be rendered voiceless. Washington is going to define what your community needs, not you. For an organization like mine, the National Alliance of Community Economic Development Associations, which represents state and regional associations of community development corporations and other community-based organizations that deploy bank resources in their communities, that’s particularly problematic and it will be a focus of ours going forward.

There are other problematic details as well, but here’s the worst part.

The rule proposes that a bank must meet a benchmark level (ratio) of investments in only a “significant portion” of its assessment areas in order to receive a satisfactory or outstanding rating. The rule suggests a “significant portion” would be defined as something more than 50 percent.

Think about that.

A bank could choose half of its assessment areas to serve, ignore the rest, and still receive an outstanding rating. Which half of a bank’s communities do you think will get left out? As my mother would say, “I’ll give you three guesses and the first two don’t count.”

Even if you’re a superfan of the misconceived one-ratio idea, you must acknowledge that allowing a financial institution to serve anything less than 100 percent of its assessment areas would legalize redlining.

. . . but 50 percent?!

When I first read “50 percent,” I was charitable in my interpretation.

“They couldn’t have meant that. I must be missing something somewhere in this rule . . . It must be my fault for not understanding.”

“This must have been an oversight.”

“This will get fixed in the rulemaking process . . . right?”

But after talking with representatives from the Federal Reserve and OCC and reading FDIC Board Member Martin Gruenberg’s opposition statement to the proposed rule, I became more and more incensed and disheartened. The fact that this 50 percent idea got this far in a rulemaking process that started on Comptroller Otting’s first day on the job in early 2017 makes several things clear.

- Comptroller Otting has a solution in search of a problem. According to career staff at the OCC, the Comptroller made CRA overhaul a priority on his first day in the office. A professional and sound rulemaking process, with something as complex as CRA, would begin with a version of the Hippocratic Oath: “First do no harm.” CRA was originally enacted to end redlining. The Comptroller’s first goal should have been to prioritize the problem CRA was intended to fix. No matter what CRA modernization looks like, AT LEAST make sure we are preserving the original intent. But he didn’t do that. He prioritized policy compliance over impact and outcomes, putting numerators and denominators ahead of families and communities. He made the policy the problem. On my first day of public policy graduate school, it was drilled into our minds that policies are not problems. In 2020, too many struggling neighborhoods—and communities of color—cannot access capital and basic financial services. THAT is a problem. And as a result of the Comptroller’s narrow-minded search to ease compliance for financial institutions, he’s proposed bringing redlining back.

- At best, community organizations are being ignored. At worst, this process was rigged against communities from the start. In NACEDA’s response letter to the Advanced Notice of Proposed Rulemaking in late 2018, we state, “Anointing a single ratio as the determining factor of CRA compliance necessarily decreases the significance of assessment areas and a financial institution’s obligation to identify and serve local needs.” Our members made similar statements in their comment letters, as did just about every advocacy organization of which I am aware. And yet, the “one ratio” remains core to the OCC’s plan. Pair that with the openly hostile relationship Comptroller Otting has had in the past with CRA compliance, fair lending and community relationships during his time at OneWest Bank, and I cannot have confidence in the Comptroller and his stated intention “to encourage covered institutions to better serve their communities, including low- and moderate-income (LMI) neighborhoods . . . that need it most.”

- The proposed rule is beyond repair. The 50 percent proposal lays bare the intentional strategy to poison the wells of the communities we serve, by giving banks a pass on serving the communities within their footprints that face the greatest challenges. NACEDA will submit our comment letter and ask others to as well. But make no mistake, this proposed rule cannot be fixed simply by changing 50 percent to 70 percent, 98 percent, or even 100 percent. While 100 percent could potentially remove the technical incentives to redline, the problems of the single ratio, the overbroad defintions of CRA-eligible investments, the gutting of communities’ voices, the speedy rule-making process, the credibility gap created by the Federal Reserve’s absency, and the lack of good faith and outreach that drove this reckless proposal would remain.

Time to Act

Those who care about the future of low- and moderate-income communities must publicly make that clear. I do not have confidence Comptroller Otting will listen, but if we speak out, others will listen. After submitting our official comments, our next step is to make our case to career officials at all three regulating agencies, financial institutions that genuinely care about the communities they serve, and members of Congress, especially those who serve on the House Financial Services Committee and the Senate Banking Committee. At some point, this rule may have to be fixed or the statute rewritten. And we will need serious people at the negotiating table.

My heart is broken. This rule would legalize, and even explicitly invite, redlining—and that is not an exaggeration. The rule offers banks an opportunity to receive an Outstanding rating while only serving 50 percent of their assessment areas. Permitting such behavior would bring us back to an era where financial institutions had the option to draw red lines around—and deny financial services to—poor neighborhoods and all neighborhoods of color. Except this time it’s worse because we understand, yet choose to ignore, history.

Though my heart is broken, and the levers of power are stacked against us, I am hopeful. The Federal Reserve may release its own version of a modernized CRA. Further, as we make rounds on the Hill and within the agencies, we often hear about the 1500 letters generated in response to last year’s Advanced Notice of Proposed Rulemaking (ANPR). As impressive as that is, I have no doubt the response to this stage of the process will be many times larger.

So write your comment (before the end of February). Ask community leaders, partners, friends, and family to do so as well. Feel free to lean on NACEDA’s sample letter (which will be released in a few weeks) or any of the other samples advocates will generate. And make your voice known to your federal elected leaders and community development allies at the Federal Reserve, OCC, FDIC, and financial institutions.

Organizations serving disinvested people and places have faced oppressive systems for decades, centuries even. It’s a fight you know too well. We have been here before and have proven our ability to achieve justice, promote prosperity for all, and give our communities voice. Comptroller Otting and the Trump administration’s rise to power is a reaction to the progress our country has made, not an indication of that progress’s direction. In this moment, it’s OK to feel disheartened, threatened, angry, or helpless. But soon we’ll have to pick up the pieces of our broken hearts and put them back together again, just as we have picked up the pieces of abandoned communities for generations. We must. So get ready. We have a fight on our hands.

Who do we write to?

Gailmarie,

Regulations.gov has the formal portal for submitting comments. Once submitted there, I recommend also sending a copy of your letter to your member of Congress and Senators.

https://www.regulations.gov/document?D=OCC-2018-0008-1515

Frank

This is outrageous……I am more more than disheartened as a community advocate and one who has had generations before me victimized by redlining. I’ve heard personal accounts by my relatives. Alas!

While the proposed CRA rules have some troubling aspects, this is not true: “Redlining Would Be Relegalized by CRA Reform Proposal.” In fact, the proposed rule states, “These fair lending laws provide the legal basis for prohibiting discriminatory lending practices, such as redlining.” Exaggeration in these matters is not helpful.