This article is part of the Under the Lens series

The Racial Wealth Gap—Moving to Systemic Solutions

In the community development world, closing the racial wealth gap is nearly synonymous with “asset building,” which in turn is nearly synonymous with “reducing the homeownership gap with a sprinkling of business ownership and matching savings programs on the side.”

Anti-poverty movements started talking about “asset-building” or “wealth-building” particularly in the 1990s, when scholars like Michael Sherraden and Melvin Oliver began to point out that income alone wasn’t enough to provide intergenerational financial security. Oliver’s book Black Wealth/White Wealth, written with Thomas Shapiro, played a major role in bringing awareness to the fact that the racial difference in asset ownership was much wider than the difference in income.

A Note to our Readers

We are using the term “racial wealth gap” throughout this series as it is the most common term. However, there are multiple racial wealth gaps.

In this series we often focus in particularly on the wealth gap between Black and white American households. There are several reasons for this—first and foremost, anti-Blackness has had significant and specific effects in this country that make that gap particularly notable, particularly persistent, and particularly well-studied. In addition, there is a lack of disaggregated data for various Asian ethnic groups and a lack of data overall for Indigenous Americans.

However, the wealth disparities for all people of color are important. As of 2019, while Black households have a median of 12 cents per $1 of white wealth, Hispanic families have a median of 21 cents per $1 of white wealth. Though the data is not equivalent, one source places Indigenous wealth in the year 2000 at 8 cents to $1 of white wealth.Though each of these gaps have some unique factors, they are also all affected by the things we cover in this series.

Since that time, interest in programs like individual development accounts (matched savings programs that could be used for homeownership, higher education, or starting a business) and in ways to increase homeownership rates has waxed and waned, but the conviction that three things—a home, a degree, and a business—were the key to closing the racial wealth gap has remained firm.

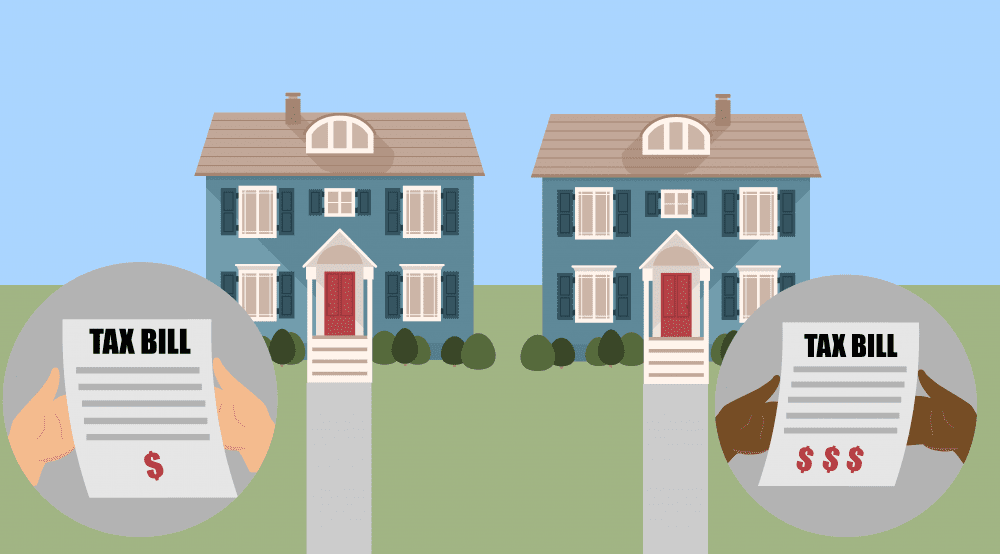

It’s not surprising that so many people have latched on to that triumvirate. These are things people of color, especially Black households, have been flagrantly kept out of in many high-profile ways, while white households leveraged them to build up large amounts of wealth. In the case of homes this was substantially accomplished by hoarding opportunity in segregated communities, and then capitalizing when that scarcity resulted in soaring property values.

But I believe that’s not the only reason why a home, a degree, and a business have such cachet. In a country that worships land ownership and entrepreneurs, markets and bootstraps, and considers homeownership the foundation of its national “dream,” calling for more access to things that will supposedly generate wealth on their own is as close to a non-controversial solution to a massive problem as you can get. They carry the elusive appeal of potential bipartisan support, and evoke our national obsession with “a hand up not a handout” and leveling playing fields without talking about how things got that way or redressing past wrongs.

That’s where we need to be careful. Are we touting only those solutions that can easily get funded and don’t make anyone with power upset, or are we looking clear-eyed at what really needs doing?

The fact is, we’ve been carrying out asset-building strategies for decades now, and though they have helped many individuals, the racial wealth gap has not shrunk. In 1983 the median wealth of white households was 8 times the median wealth of Black households. In 2016 it was 10 times. Black households lost 48 percent of their net assets in the Great Recession, and Latinx households lost 44 percent, compared to the 26 percent white households lost—and households of color have experienced less of a recovery in the years since as well.

In 2018 the Ford Foundation, which had invested heavily in scholars of color who were researching the racial wealth gap and bringing it to the public consciousness, conducted an evaluation of its work in the racial wealth gap arena. The evaluation found that individual asset-building programs, while beneficial to participants, were not successful as a method for society-wide change.

“Unfortunately, many individuals and organizations that focus on the [racial wealth gap] continue to approach the issue through an asset-building lens, which obscures the structural components of wealth inequality and the systemic levers that could be pulled to address it,” evaluators wrote.

As important as homeownership, business ownership, and higher education are—and make no mistake, we should not accept racial disparities in any of those things—we must go beyond simply promoting more of each if we want to make a difference. In this series, “The Racial Wealth Gap—Moving to Systemic Solutions,” Shelterforce widens the lens on the racial wealth gap and what needs to be done about it. We hope to help our readers form a more complete picture of what’s causing the racial wealth gap (though we won’t claim to address every possible contributing factor), and to wrestle particularly with what kind of role homeownership really does play in this process, and the role it could play with the right tweaks.

We’ll explore why we need systemic solutions, why we must stop extracting wealth from Black communities before asset building becomes truly possible, and why “homeownership is the top way to accumulate wealth” is too simplistic a statement.

The racial wealth gap is a multifaceted problem, and it will take multifaceted solutions. The first step toward making real change is being diligent not to oversimplify either the problem or the solutions.

I’ll go against the grain & complain about using “communities” or “people” “of color”. This phrase has gained a lot of traction, but it is our modern form of “separate but equal”. Using this conceptualization, pls explain ur community or economic development ideas & strategies in the context of a “separate but equal” construct bc this is the framework you are working in.

Why did you mention the Holy Trinity? Can you explain that? Because I’m a believer of the Holy Trinity.