This article is part of the Under the Lens series

The Racial Wealth Gap—Moving to Systemic Solutions

Yorktown is a slice of middle-class Black suburbia in the middle of Philadelphia, where leafy cul-de-sacs and comfortable yards were modeled after the segregated white suburbs being built on the city’s edge. For generations, it’s been the address of choice for lawyers, former mayors, and proud homeowners.

Yet when one resident had her home appraised, the value came in unusually low. Why is that? “This particular appraiser did not know this neighborhood,” says Ira Goldstein, president of policy solutions at The Reinvestment Fund, who has interviewed several Yorktown community members and realtors in his research. “He came in from out of town or in the suburbs and just took [comparable sales] that were nearby” in a more economically depressed section of North Philadelphia. “He didn’t know the neighborhood well enough to create an appropriate appraisal.”

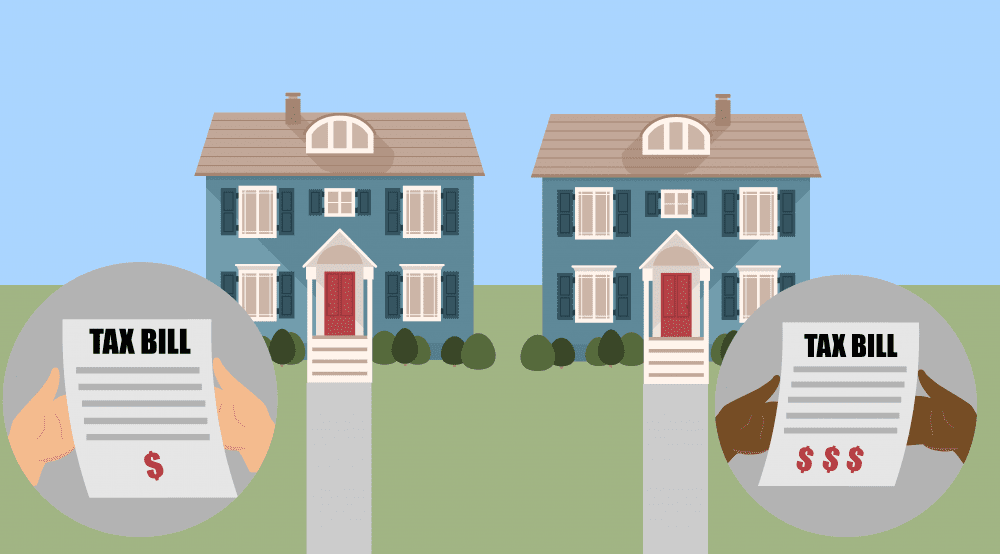

Property values in the United States have risen dramatically in recent years, the result of a one-two punch from the COVID-19 pandemic and a chronic housing shortage. Yet many Black homeowners won’t get to financially benefit from those rising prices due to “appraisal bias,” the phenomenon where homeowners of color receive significantly lower valuations for their homes compared to identical homes owned by white families.

In recent years there have been more and more stories in the media about Black homeowners who have received low appraisals. When it happens, the homeowner often has their home appraised a second time, but takes down their family photos and/or asks a white friend to stand in for them, and then discovers that their home has magically increased in value.

Undervaluing a property based on a homeowners’ race is theoretically illegal, as appraisers—like all other professionals in the real estate industry—are prohibited from discriminating by race. But the practice appears to be so widespread that a recent study from the Brookings Institution has found that homes in Black neighborhoods are valued on average 23 percent less than comparable homes in white communities, controlling for amenities like schools, safety, and walkability. In other words: A home in a prosperous Black neighborhood is still only worth as much as a home in a disadvantaged, but predominantly white, neighborhood.

That comes to about $156 billion in lost equity nationwide, says Andre Perry, a senior fellow at Brookings, who led the study. “It may not mean a lot to some people, but it would have financed more than 4 million Black-owned businesses,” he says. “It would have paid for more than 8 million four-year degrees. It would have replaced the pipes in Flint, Michigan, nearly 3,000 times over.”

Unlike other segments of the real estate profession, the appraisal industry tends to be insular and difficult to enter. For example, a real estate agent needs only to take a class and pass a licensing exam, but appraisers must receive thousands of hours of apprentice training alongside a more experienced professional. As a result, the industry is fairly homogeneous and experiences little turnover: 85 percent of appraisers are white and 77 percent are male, according to the Appraisal Institute, and 70 percent of appraisers have been in the profession for at least 15 years.

That system means that many new appraisers are receiving training from appraisers who started their careers at a time when racist standards were the norm. As late as the 1970s, now-discarded appraisal guidebooks “made race an explicit factor in determining value,” says Greg Squires, a sociology professor at George Washington University who has researched the appraisal gap. Older appraisers, simply by virtue of their personal or professional experience, may lack familiarity with urban or predominantly Black communities and so are unable to pass that knowledge on to their charges. And as most appraisers are sole proprietors, they may never get exposure to other appraisers who are familiar with those areas.

“Even if an appraiser does everything 100 percent correctly according to the rules, they likely bake in that history of discrimination that’s already encapsulated in the comparable sales,” notes Goldstein.

the ripple effect

In 1977, the Community Reinvestment Act outlawed practices, like redlining, that mortgage lenders used to discriminate against borrowers of color, but the legacy of those practices remains. Today, 43.1 percent of Black families are homeowners, compared to 74.4 percent of white families. Black families have on average one-tenth as much wealth as a white family. Despite considerable anecdotal evidence, housing researchers don’t have a lot of data about appraisal bias, or its contribution to the racial wealth gap.

Perry’s research validates what both homebuyers and housing providers have seen for decades. “We hear about this from so many [homeowners],” says Sarah Brune, housing policy director at Neighborhood Housing Services, a Chicago-based group that provides loans and counseling to buyers with credit or financial issues. “Yet when we meet with some of these stakeholders and decision-makers they say ‘We know there’s data, but we’re not hearing about it.’”

Neighborhood Housing Services and Chicago Rehab Network, a coalition of housing organizations, are surveying Black and Brown borrowers about their appraisal experiences. One common theme of the responses is that low appraisals discourage residents from investing in their homes. “If someone can’t borrow money to fix up their home, just basic repairs, you see deterioration of homes and buildings,” Brune says. Or homeowners may use cash to fix up their home instead, “which doesn’t get recorded anywhere, so they may have put $100,000 in the home but it’s not $100,000 that the appraiser ever sees.”

That causes a ripple effect. “A lot of different interests depend on having accurate assessments of property values and when you don’t have them, lots of people lose,” notes Squires. “Real estate agents lose their commission. The bank loses the fees from their mortgage. The homebuyers were going to buy some appliances or do some landscaping on the home, and now they won’t. Property values can be depressed. Property tax revenues can be reduced. Jurisdictions have fewer dollars to provide public services.”

Thus, a cycle forms in which entire communities are deprived of wealth and opportunities to build wealth. Without equity in their homes, Black homeowners are denied a source of funds that white homeowners commonly use for education, home improvement, and other life enrichment, or to use their home as collateral for things like business loans.

moving to accuracy

As appraisal bias gains more attention, some solutions are coming into focus. A crucial first step is consumer education—helping homebuyers understand their rights if they receive a biased appraisal and where they can report discriminatory actions. Rachel Johnston of the Chicago Rehab Network says this is crucial to combating appraisal bias. “What we’ve found just from talking to neighbors and friends and colleagues that people of color who’ve had appraisal issues is it’s not clear how to complain,” she says.

Squires recommends looking at appraiser training and vetting—such as programs from the Appraisal Institute, the nation’s largest professional association of appraisers—and replacing the apprenticeship period with formal education and a standardized curriculum so new appraisers learn current standards and practices. That may also make training more accessible to people who don’t have the social connections to get an apprenticeship. And just as cities or organizations have preferences for minority-owned contractors, they could also create lists of preferred appraisers who identify as people of color or who have a history of serving communities of color. “There’s a financial incentive for appraisers to do that kind of work and to train appraisers to serve those kind of communities,” he says.

Changing how appraisers value properties is another solution.

Traditionally, appraisers look almost exclusively at similar homes in the immediate area that have sold within the past few months, which provides a limited view of a home’s worth. Instead, Goldstein suggests looking at how much rent a property could generate, based on findings that homes in cities like Philadelphia or Baltimore could be considered worth $20,000 but still rent for $1,200 a month, a significantly higher rate than the home’s value would indicate. “That’s likely going to be to the advantage of someone trying to sell and get a more accurate appraisal in lower-priced areas,” he says.

Increasingly, lenders are simply taking appraisers out of the process. Two years ago, the Federal Housing Finance Agency gave lenders more freedom to use automated valuation models (AVM), which have an algorithm that calculates a home’s value based on a database of home sales, and can be used alongside an in-person appraisal or as a replacement for one. While the decision was partially intended as a safety precaution at the start of the pandemic, it can also address bias. “Any personal bias someone might bring to the property is gone if it’s an automated value model,” says Goldstein.

But the algorithm’s effectiveness in combating discrimination may depend on what data is used. A recent study from the Urban Institute found that AVMs can produce significant pricing errors, either too high or too low, that perpetuate racial disparities in home values. That’s because as with in-person appraisals, AVMs today continue to use comparable homes in a single neighborhood.

That approach just “recycles the discrimination over and over again,” argues Perry. Instead, he recommends AVMs that use data for an entire metropolitan area, comparing a home to any homes in that region of a similar size, with similar features, or in a similar type of neighborhood. Using that approach, if a home in a Black neighborhood were compared to a similar home in a white neighborhood with similar education and crime rates, its value would be significantly higher than it would have been under the old method.

While that increase in value would benefit current homeowners, Perry recommends simultaneously directing financial resources, like downpayment assistance or tax credits, to homebuyers to ensure that they aren’t priced out by a shift in appraised values. “We shouldn’t just change values without restoring some of the value that’s been extracted by racism,” he says.

A HUD task force that focuses on equity in home appraisals is expected to release a report early this year on ways to end appraisal bias, with a focus on government oversight and consumer education. The task force, established last summer, brings together over a dozen federal agencies along with appraisers and fair housing groups.

The goal of ending discrimination in appraisals, say housing advocates, is to improve outcomes for both consumers and communities.

“We’re not setting out on this work to demonize any individual or any industry,” says Brune of Neighborhood Housing Services. “It’s more about recognizing the policies that led to the racial wealth gap today and talking about how we can change the process of conducting appraisals and the many factors that go into real estate valuation.”

Comments