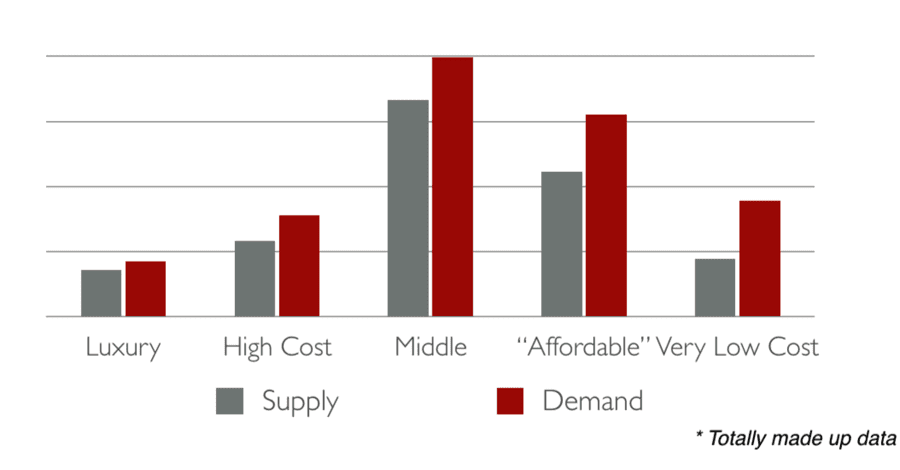

Liam Dillon covers the politics of housing policy more closely and thoughtfully than almost any other journalist in the country and yet he was nearly dumbfounded by the results of a recent survey commissioned by his paper, the Los Angeles Times. The Times and researchers from the University of Southern California asked 1,200 California residents about the causes of the housing crisis. Only 13 percent of respondents blamed the crisis on “too little homebuilding.” Twice as many people included “lack of funding for affordable housing” or “lack of rent control” as top explanations for the problem.

why is housing in california so unaffordable?

Dillon sought comments from experts who struggled to explain the results; they all agreed that the lack of supply is at the root of the problem. Democratic state Sen. Scott Wiener, who has been leading a truly impressive crusade to get more housing built in California, said it will take time to convince Californians of the housing shortage.

Wiener wasn’t the only person who focused on persuading the public. Both in the comments section on the LA Times website and on Twitter, commenters wondered what it was about supply and demand that voters can’t quite understand. More than one person suggested that all voters be required to take an entry-level economics class.

Given the enormous gulf between the view of Dillon’s experts and the majority of voters, one reaction that was conspicuously missing from the overall response was curiosity. Isn’t it possible that voters understand something that the experts are overlooking?

For the record, let me say that I generally believe the experts: In places where there is high demand, we need to build more housing—subsidized and market-rate housing, and even some luxury housing. It won’t solve the housing crisis on its own, but we can’t solve the crisis without building. So how do we make that happen? We will only see significant increases in the pace of development when the public broadly begins to agree that they are better off with more building than with less. Winning people over to that point of view won’t be easy, but telling people that they are stupid and uninformed is definitely not the right place to start.

It seems to me that if we want to convince people, we ought to stop yelling and start listening.

why aren’t voters buying the need for more building?

This survey perfectly captures the bind that elected officials across the U.S. find themselves in these days. A new breed of YIMBY (Yes, in My Back Yard) activism and academic analysis have together helped big city governments take the first lumbering steps toward higher rates of housing production. We are building more than we have in years. But for the most part, the average voter remains highly skeptical that market-rate real estate development can make a positive difference.

If you are in the group that finds the need to build more to be intuitively obvious, you may be more than a little put out by the LA Times survey results. You may be tempted to wonder why so many people refuse to believe that supply and demand will work the way it works in Econ 101?

In any introductory economics class we learn that supply and demand interact to set prices. If we increase demand (e.g., more people want to live in our cities), the price of a good will rise. In most markets, rising prices will encourage producers to make more of the good in demand, and increased supply will bring prices back down.

In the Econ 101 view, any new unit has the same impact on average rents. It doesn’t matter if the new unit we add sells for many millions of dollars; the household that moves into it vacates another unit, which is then available for someone who earns less money. The process works its way down through the whole economy and everyone, everywhere shares in the benefit.

But a surprising number of people shrug this logic off. William Marble and Clayton Nall in the Stanford University Department of Political Science wanted to see what it would take to change people’s minds on development. They surveyed people in the 20 largest metro areas and found that people formed attitudes toward new development independently from their overall political ideology. Many people who identified the need for housing affordability as an important issue opposed new development. Marble and Nall guessed that if they first provided people with information about how development leads to more housing affordability, people would answer survey questions about development differently. But they found that no matter what message they started with, people’s answers didn’t change. It didn’t help to say that experts agreed, it didn’t help to say that evidence showed that low-income people would benefit, and it didn’t even help to say that President Barack Obama endorsed the research. This finding highlights the challenge facing policymakers; no amount of public education is likely to make a difference. Urban voters seem to understand the argument but remain unpersuaded.

My view is that this tenacity is not the result of a lack of understanding or education. Instead, I think it grows from a sensible feeling that the Econ 101 story greatly overstates the extent to which lower-income people, and even middle-income people, will benefit from luxury development. It is hard for people to articulate this feeling given the degree to which the whole discussion has accepted the simpler premise. And while I believe that resistance to development is causing great harm, particularly for lower-income people, I don’t think we can overcome that resistance without addressing the real question that people are raising. To do that we have to look more closely at who benefits most from new development and think a little harder about what steps local government can take to share that benefit more widely.

what about everything after econ 101?

One reason this debate is so frustrating is that Econ 101 is not the right class for housing policy. Housing is different from other goods and services in a number of very important and mostly well-understood ways. And because of this difference, housing is not generally covered in undergraduate economics courses. Housing is advanced economics.

If we’re going to agree on a course of action for housing affordability, we really need to first agree on how the economics work. But we won’t get the policy right by agreeing that the economics are simpler than they really are.

I have spent much of the past decade in the middle of fights over housing production in big cities across America. After one too many debates where both sides seemed to be making up their economic theories on the spot, I decided to look into what the academic research said about the impact of housing production on rents. I learned quickly that there are some questions that Google can’t answer. One reason it was hard to find relevant research is that these questions were the focus of economists in the 1970s and 1980s and many of the relevant papers are not available online. One economist I spoke with said, “Once economists come to a satisfactory answer to a question, people simply stop studying it.”

Starting in the 1940s, economists began to explore the ways that housing markets were different. Housing is immovable and very expensive relative to other goods, people incur significant costs when they choose to move homes, and characteristics of the neighborhood that their home is located in seem to matter as much as the homes themselves when it comes to setting prices. By the 1960s, some economists began to document the process of filtering and to develop theories that would predict how home prices and rents would be impacted by new construction.

By the late 1980s, a group of economists led by Jerome Rothenberg and George Galster undertook an ambitious effort to bring together much of this research into a single economic model of the housing market that would be realistic enough to address the questions facing housing policymakers. They published a series of articles and a textbook, The Maze of Urban Housing Markets, which was described by the publisher as “a powerful new theoretical approach to analyzing urban housing problems and the policies designed to rectify them.” It seemed like they had answered the core economic question once and for all. But even though there has been very little pushback from other economists, this framework does not seem to have changed how we approach housing policy. Probably because only a small number of students in graduate-level housing economics classes have ever heard of this work.

But it’s time to take another look at this research because it directly addresses the specific questions that paralyze policymakers and elected officials today. This approach suggests a view of both the power and the limitations of new development that is dramatically at odds with the point of view that the LA Times described as being shared by all the experts.

the housing market is segmented

The authors of The Maze of Urban Housing Markets analyzed data from dozens of U.S. cities and came to a surprising conclusion: The housing market is segmented. The structure of urban housing markets is better understood as a set of interrelated submarkets that can move somewhat independently than as a single market. It takes a little time to get used to talking about housing this way, but my guess is that when you think about it, you’ll realize that you already see it this way even though it’s not how you generally talk about it.

Think about the price of gasoline. It varies in different parts of the country, but in any given city, gas prices vary only a small amount. You may be willing to pay a few cents more to buy gas from a name-brand station or one closer to your home, but if the prices were much lower somewhere else, people would go there because, let’s face it, gas is gas. The website gasbuddy.com tracks gas prices all across the country. In California, a gallon of gas costs more than $3.50. At the same time people are paying $2.15 or less in parts of Texas. But within any one city, the prices tend to vary by 10 cents or less between stations. In other words, the national gas market is divided into regional submarkets with prices that adjust somewhat independently, but within any one city there is a single market for gas.

Now, compare that with apartments. Obviously the national apartment market is also segmented into different regions where prices move independently. But what about within each city? Sure, we can calculate the average rent for a two-bedroom apartment in each city, but depending on who you are, you might pay a lot more or a lot less than that average. Gas may be gas, but apartments aren’t all the same. The most desirable units in the hottest neighborhoods will cost many times more than the least desirable apartments.

But most apartments aren’t quite unique either. If you rent, my guess is that you looked at less than 10 available apartments before you signed a lease, even though there were hundreds more available in the area. By looking at only a few places, you got a clear sense of the current market price for the kind of apartment you were looking for in the kind of neighborhood where you were looking. And that general sense held up across many slightly different units. There was a market and a market price even if it was not a single citywide market. In a segmented market, the price you pay for an apartment is still set by supply and demand, but it’s not just the overall supply and demand that matters. The rent is at least partly set by the supply of apartments like yours and the amount of demand from people like you.

It’s tempting to think that the issue is just geography: that apartments are just like gas, but instead of different markets in different states, there are different markets in each neighborhood. Clearly neighborhoods are important, but the research suggests that both location and other quality factors and building amenities combine to define distinct submarkets. You can think of each submarket as all of the different units that one kind of person might consider when they are looking to move. They may be in several different neighborhoods, but they will be of similar overall quality and desirability and they will have similar prices.

It’s easier to see how this works if you think about student housing. Student units have to be somewhat close to a university and be available to rent by the academic term instead of the year. But not all housing near university campuses is student housing. You can often tell the difference from the street because, apparently, students don’t care about landscaping. In some neighborhoods, two different markets—student and non-student—operate side by side on the same block.

Like any product, the rent for student housing is determined by supply and demand, but it’s mostly the supply of student housing and the demand from students that matters. When a university’s enrollment drops, the rents for student housing drop because student-housing vacancies rise. If they fall enough, landlords may convert some student housing to housing for other people. But that change will come with a cost. For one thing, the landlord may have to invest in landscaping, not to mention kitchen and bathroom remodeling. So student housing is a distinct submarket. Because housing units can be moved into or out of the student submarket, the student prices are not fully independent from the non-student market.

Rothenberg and his colleagues found that the student market is not unique in this sense. They saw a similar pattern in every community. Housing markets were segmented by quality and the supply and demand in each submarket resulted in semi-independent price movements. A community might see rising prices in the high end of the market even as prices in the middle or at the bottom were falling. And vice versa.

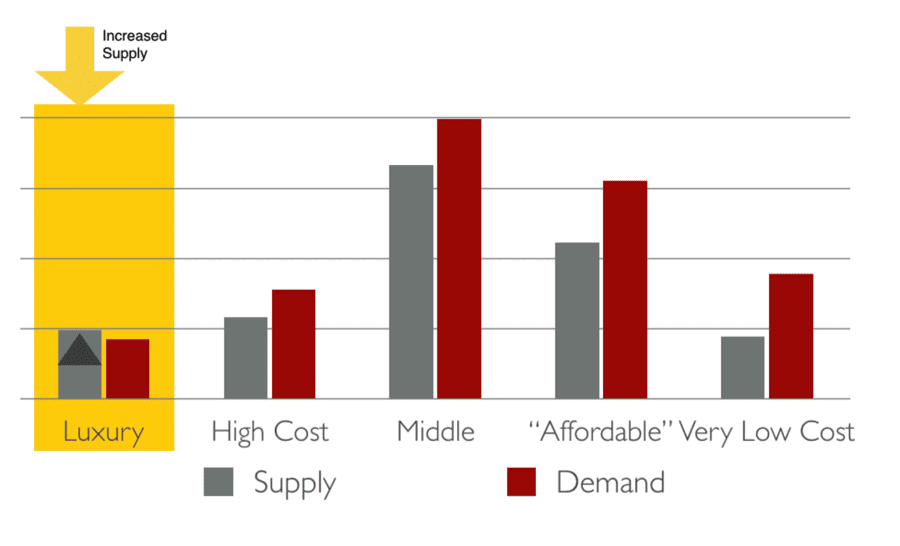

They considered how housing markets that were segmented in this way would respond to a range of different changes in supply or demand in any one segment. One scenario that they evaluated most closely was the situation where new housing was added at the most expensive end of the market. What they found was that when new luxury homes are built, there is an immediate response within that specific submarket. Prices drop in response to increased supply just as we would expect from Econ 101.

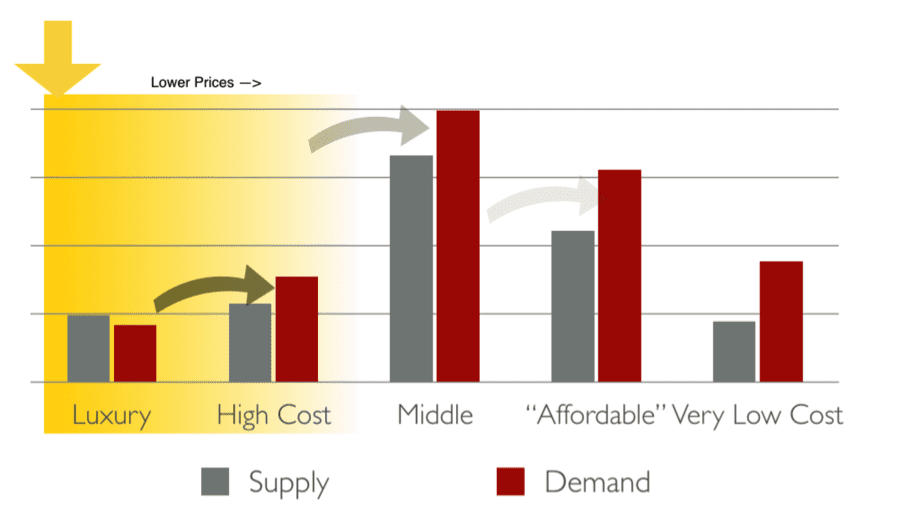

In the next subgroup down market, prices fall also, but not by as much. When luxury prices drop, some people will upgrade from merely high-cost housing into the luxury market. This reduces demand in the high-cost submarket, which lowers the price. But for a number of reasons, each new luxury unit was associated with less than one household stepping up. So the price reduction is less in the second tier. And for each step further down, the effect of the added supply was diminished to the point where the addition of new luxury housing made relatively little difference to the rent for low-cost housing units.

the most important number you have never heard of

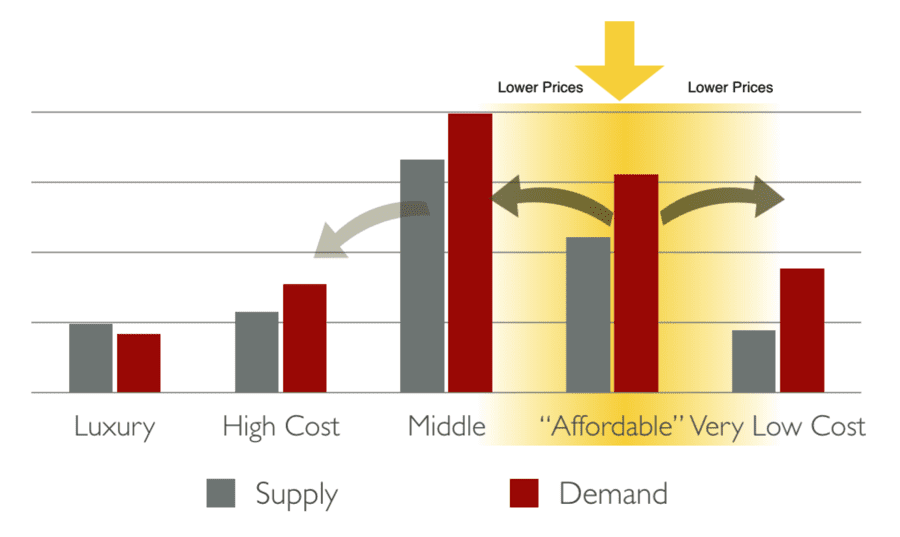

If markets are indeed segmented in this way, then the results of the LA Times survey may make somewhat more sense. Why are people in Los Angeles not excited about the potential for new luxury development to make all housing more affordable? For the same reason they don’t see new buildings in Seattle or Portland helping them. Surely it is at least partly true that the more Seattle builds, the less pressure there will be on California’s housing markets. (Lower prices in Seattle will cause some people to move north.) But we all intuitively understand that this will make only a very small difference in the cost of housing in LA. New luxury towers in the city seem no different to many Los Angeles residents, who feel like they occupy an entirely different world.

Of course, new buildings in LA (even luxury buildings) are likely to have a much bigger impact on middle- and low-income rents in the city than any buildings in Seattle. But, sadly, it turns out that we don’t know how much bigger. The key number is what economists call “cross-price elasticity of demand,” a measure of how readily people switch from one submarket to another.

“Elasticity” is the kind of jargon that keeps economists in business. “Elasticity of demand” is the extent to which the quantity of a product that consumers demand changes as the price changes. For most products, if we lower the price, people buy more; elasticity is the measure of how much more. If a good is highly elastic that means that it is price sensitive—a 10 percent drop in price will result in more than a 10 percent increase in the quantity demand; a 10 percent increase in price will cut demand by more than 10 percent.

A cross-price elasticity of demand (XED) instead measures how a change in the price of one product impacts the level of demand for another product. For example, if the price of gas rises, the demand for public transit increases. Driving and transit are what economists call substitutes—you can trade one for the other— but they are not perfect substitutes, which means that even when gas prices spike, transit ridership only rises a little. In this case, economists would say the cross-price elasticity is less than 1.

Similarly, economists have studied the cross-price elasticity of demand for butter and margarine and estimated it to be .66. This means that if the price of butter falls by 10 percent, then margarine consumption will fall, but only by 6.6 percent. Some people are buying margarine because it is cheaper than butter, but some people just prefer margarine.

why does this matter?

If housing markets are segmented, then when we build more luxury housing, the price of luxury housing falls (Econ 101). But if each new luxury unit does not correspond to one less household in the next market down (the ‘high-cost’ submarket), then the prices in the high-cost market will move less noticeably than the luxury prices.

Why wouldn’t there be a 1-1 change? For every new luxury unit, doesn’t someone vacate a less expensive unit down market? Not exactly. There are many reasons why the submarket units are imperfect substitutes. For one thing, as prices fall, households in the luxury segment of the market may consume more housing. This can happen when someone buys a second home or even when two roommates respond to lower prices by each renting their own place. But also, some luxury units may be taken off the market when prices fall, while others may be downgraded to lower-quality buildings because the lower rents may no longer be enough to support luxury amenities and services. There are a great many possible permutations, but at each stage in the process, adding one unit or removing one household from one tier does not automatically mean that one additional household will step up into that tier.

I think it is clear from this that we can’t expect new luxury development to have the same impact on rents at the bottom of the market as it does at the top. But how much less impact is not clear. In technical terms, there is no good recent data on the cross-price elasticity of demand between luxury housing and lower-cost housing. A large group of urbanists have taken to talking about the housing market as if these elasticities were close to 1 (increases in luxury supply have a big impact on the low-end rent). But it’s just as likely that the elasticity is closer to 0 (the rent at the bottom of the market is very insensitive to the level of supply at the top of the market).

One of the things that I find most striking about this way of thinking is how much the list of things that might cause the XED to be much lower than 1 looks like the list of concerns you hear from people who don’t see new development as the key solution to the housing crisis. There has been quite a lot of pushback against new development on the grounds that many units are sold to Russian oligarchs or other foreign investors. By itself, this is a spectacularly weak argument against building because the total number of oligarch units is so low. But taken together with other factors, it seems like just one more way the benefit of luxury development never quite reaches the masses.

Similarly, people like to complain that new apartment buildings are mostly made up of studios and one-bedroom units. In an unsegmented view of the housing market, this should not matter because the people moving into these units will vacate units somewhere else in the city. But, if we see the market as segmented, then it matters that new buildings are serving young single people because we can expect to see the biggest price impacts on other housing that those singles would have occupied. Other young singles will get most of the benefit. When you look at all of these complaints together, they paint a picture of an electorate laser-focused on the one number that really does matter: cross-price elasticity of demand.

So much depends on this one number. If the elasticity is 1, then all new building is inherently good for everyone equally and we should build as much as possible without worrying much about who we are building for. At any point below 1, luxury development is most beneficial for the rich and less helpful for everyone else. Below 1, any policy that results in new buildings that serve the middle of the market will increase the degree to which middle- and-low income people benefit from building. At some point we get far enough below 1 that luxury housing development stops looking like a reasonable solution to the housing affordability problem at all. At that point, other strategies, like subsidized affordable housing, start to seem like more obvious solutions.

what should we do?

There is a meaningful debate about whether new developments push rents up or down in the neighborhoods immediately surrounding them. My view is that there are sensitive neighborhoods where fancy new buildings can accelerate gentrification, but there are also many more neighborhoods where that is not much of a risk. At the regional scale, there seems to be wide agreement and strong evidence showing that more building leads to lower average rents. But the average rent does not tell the whole story; who we build for seems to matter. If we build only high-end housing, everyone may see some benefit, but most of the benefit will flow to the rich. Low-income people may (depending on XED) receive very little benefit. Of course, if we don’t build at all, no one benefits. So, in some very real sense, some building is better than no building. But we have more options.

The most compelling policy implication of this switch to a segmented view of housing markets is that we need to do more to encourage development of new buildings that are targeted for lower- and middle-income households.

We invest a significant amount of public money in subsidized affordable housing—primarily through the Low-Income Housing Tax Credit program. We tend to justify this investment primarily based on how those buildings affect the families who live in them. But think about how adding new supply at the lower end of the market impacts the rents that everyone else will pay. Just like with high-end housing, the benefit accrues most noticeably within the same sub-segment of the market where new building happens. When we add lower-income units, we increase the supply and reduce competition for lower-cost housing and the benefit filters out in both directions to help people renting in the market segments just above and below. People at the top of the market receive the least benefit from this kind of new supply.

listening to voters

If we accept that the market is segmented, then it matters who we build for. In one obvious way, that is bad news. Building for the rich is simply much easier than building for anyone else, given the high construction costs. But for policymakers who are struggling with how to get more housing built, this should be very good news. If it matters who we build for, we can do something about that and we can get the great bulk of voters behind that kind of action.

Yes, local governments in hot market areas must take bold action to enable more development, but it matters to voters what kind of development results and, specifically, who that development is for. Instead of (or in addition to) focusing on changes that support development in general, we should identify the policies that change who benefits from new development and we should stress that aspect when we explain these policies to the public.

Changing who benefits is not easy or inexpensive. But the research on public attitudes suggests that even small changes along these lines can make a big difference.

Michael Hankenson, a graduate student at Harvard, surveyed renters in high-cost urban markets. He found widespread opposition to new development with a majority supporting an outright ban on new building in their own neighborhood—even among people who claimed to support the need for building more housing generally. But, among renters, attitudes toward affordable housing were quite different. While renters were less likely to support market-rate housing the closer it was located to their house, for affordable housing the result was reversed. People supported affordable housing more strongly the closer it was to their home. And, surprisingly, this difference was exactly the same for projects that were 100 percent affordable and those with only 25 percent affordable housing. Including a share of affordable units in primarily market-rate buildings dramatically changed people’s attitude toward the project. Hankenson didn’t test levels of affordability below 25 percent, but the popularity of inclusionary housing policies in cities across the country suggests that this is a common reaction and it is relevant even at much lower shares of affordable housing. People want to support development when they see it as not exclusively benefiting the rich.

growing bottom-up housing policies

One clear implication of this perspective is that we need to do even more to support development of income- and price-restricted affordable housing units. These units add to supply from the bottom up. New units come directly into the submarkets where they will make the most difference. But this is not news to local policymakers. More and more cities and counties have, in fact, been identifying local funding sources to subsidize affordable units. This is the right first step and hopefully a trend that will continue. But there is also a limit to the extent to which local taxpayers are likely to fund affordable housing development—however much they may acknowledge the problem. Ultimately only the federal government can realistically fund a large-scale expansion of affordable housing development.

Similarly, nearly every major American city has now adopted some form of inclusionary housing—requiring, or in some cases incentivizing, developers to include below-market-rate units in new market-rate buildings. But there is a limit, and sometimes a fairly low limit, to how much affordable housing can be included in a project before it is financially infeasible to develop at all. Cities however, are not powerless against this economic reality. Local planning and zoning regulations have enormous impact on what and where it is financially feasible to build. Time and again, urban voters have shown a willingness to trade relaxed density rules or reduced parking requirements in exchange for more affordable housing units.

The same voters who are consistently skeptical of market-rate building for its own sake seem to have no reservation about using market-rate development as a tool to get more affordable housing. The experts have had little success in convincing voters to remove restrictive zoning rules for the sake of more building in general, but there is a proven track record of doing exactly that in exchange for more affordable housing units. Pursuing regulatory reform on its own in the absence of clear requirements for affordable housing is not a good use of energy. It might pass in the state house, but the LA Times survey shows why someone in every city hall is going to try to fight back. However, when we tie reducing regulations to affordable housing requirements (of almost any kind) we can all pull in the same direction.

experiment with middle-out housing policies

Where the policy choices become truly difficult is when we move up the income scale to think about more middle-income housing. If markets are segmented, then building middle-income housing would be vastly more helpful than only building luxury housing because instead of filtering from the top down, the benefits would filter from the middle out. While the market is unlikely to ever provide high-quality, low-income housing without public subsidy, in the past the market did provide plenty of middle-income housing and it could again.

In the early 20th century the federal government’s early interventions in the housing market focused on supporting the creation of market-rate, middle-income housing. Federal mortgage guarantee programs reduced the risk and cost of building. And many cities have issued bonds to finance middle-income apartment buildings. These programs can be abused, but they show that local governments can take an active role in ensuring that financing is available for new production of housing that serves more middle-income segments of the market.

And there is also growing interest in changing design and development standards to make it easier to build for the middle of the market. The recent growth of accessory dwelling unit programs can be seen as one way to do this. Several cities have been considering legalizing fourplexes in single-family neighborhoods. While these changes don’t guarantee that new housing won’t be expensive, if they are implemented at a sufficient scale, it is likely that the new units will be much more modestly priced than most multifamily development has been. Even if these new units don’t directly serve lower-income households, their benefit is more likely to reach the lower end of the market because they will start closer to the middle than much of the multi-family housing we have been building in recent years.

living with supply skepticism

Time and again, housing policy ‘experts’ in this country have helped rationalize and implement policies that enriched property owners and real estate investors at the expense of communities, particularly those of color. We bulldozed people’s homes. We wrote racism into the zoning code. We promoted harmful financing scams. Our collective failure to own up to these past harms is a surprisingly central force driving the current housing shortage. Many people simply aren’t inclined to trust the experts any more.

But it is easy to overlook the many times when the partnership between the public sector and the real estate industry worked the other way. At the beginning of the 20th century, most Americans lived without indoor plumbing, fires regularly leveled whole neighborhoods, and substandard and overcrowded housing was a major contributor to deadly epidemics. Private builders all but eliminated some of those concerns from our public life. Builders didn’t install fire-rated walls or sprinkler systems to save money. They did it because laws informed by the experts made them. Homebuilders didn’t invent the 30-year, fixed-rate mortgage to help middle-income people afford homes. Experts inside the federal government did.

Urban voters aren’t likely to embrace a strategy of getting out of the way and letting the market do its magic. Many are inclined, instead, to stand in the way to keep the market from doing harm. But if we were more honest about the limitations of the market, it would be easier to convince people that local governments can hold private development accountable for delivering benefits to people who are being left out.

This is a terrific article, deserves wide distribution! One missing element is a discussion of the role of filtering: the bump-down over time of aging units from one market segment to the next as the shine wears off. So the apartment complex built as upper-middle housing becomes middle income in 10-15 years, and affordable in 20-25 years. This depends on neighborhood dynamics and owner strategy also. An older project in an in-demand neighborhood can maintain its position with renovation.

“depends on neighborhood dynamics and owner strategy” – key point.

5th Ave. in NYC was expensive before 1900, has been expensive ever since.

I am hard pressed to think of many areas where this idea of Expensive becomes Cheap happened. I think it is YIMBY “fake economics” but am open to examples where it applies. Got any?

North Broad in Philadelphia is the example I’m most familiar with, but Brush Park in Detroit is the most iconic example. In both cases, however, we’re looking at neighborhoods built for the very rich that experienced extreme downfiltering — that is, they became their city’s worst slums. (Both neighborhoods are currently experiencing gentrification.)

I am sure that, if you look into the history of your city, you can find a similar example. Neighborhoods like the Upper East Side (NYC), Rittenhouse Square (Philadelphia), or the Gold Coast (Chicago) appear to have been exceptions, rather than the norm. Indeed, downfiltering of urban markets was so pervasive and extreme that even middle-class urban neighborhoods had become rare commodities in several cities (e.g. Cleveland) and outright nonexistent in others (e.g. Detroit) by the late 20th century.

Jacobus is telling us that the building of market rate luxury housing doesn’t help in the short run. It does 30 years later.

I don’t get it. Why does the benefit filter out in both directions?

@j

some people who would otherwise select more luxury might be willing to settle for a lower quality unit for other reasons like location of the lower cost unit, thus increasing luxury stock slightly.

What exactly does it “luxury housing” mean? Here it sounds like you mean anything expensive, but in the Bay Area where I live most new apartments are expensive because they’re new and there’s a housing shortage. There’s nothing about the way they’re designed that should make them as expensive as they are. The same apartment in Texas would be half as much. The only reason the market is segmented as such is our housing shortage.

There is no housing shortage in California. Housing is expensive in desirable places where people make a lot of money because the people with a lot money out-bid the people with less money who commute from further out. They in turn outbid those with even less money who commute from even further out.

“First an increase in the population size has fairly straightforward effects. Indeed, a rising population makes competition for land fiercer, which in turn leads to an increase in land rent everywhere and pushes the urban fringe outward. This corresponds to a well documented fact stressed by economic historians. Examples include the growth of cities in Europe in the 12th and 19th centuries as well as in North America and Japan in the 20th century or since the 1960s in Third World countries.” (From page 83 section 3.3.2: Economics of Agglomeration:… by Fujita, Thisse).

More on Urban Economics here:

https://meetingthetwain.blogspot.com/2017/04/urban-economics.html

I love this. Thank you for working to fuse the politically feasible with the economically justifiable. I see a corollary in carbon pricing which has widespread economist support, but thus far seems to lack political traction due to concerns about fairness. My hope is that carbon pricing will take off once it is a component of a plan that clearly produces tangible benefits that address the underlying concerns about equity. Similarly, we have to crack this nut of ensuring that a massive increase in housing production is part of a process that clearly addresses voters’ concerns about equity.

Thanks Anonymous,

I think that breaks down in areas where the physical structure is 10% of the cost, and the location is 90%. The lower-quality unit is at a luxury cost, not an “affordable” or low cost. It’s luxury stock because of the location, not the quality.

As is most of the immediate coastline. I live in an area where people literally buy a house and then take it down and put in what they want instead.

Maybe voters don’t believe in supply and demand because they’ve been told for the last twenty years that adding 7.5 million people to the state’s population doesn’t cause school crowding, doesn’t mean there’s more competition for jobs, and doesn’t cause rents to rise. So if all these things are true, then it must also be true that adding more housing won’t have any effect.

So much common sense here. And, yes, this deserves wide distribution. Thanks!

ON THE PA: “All YIMBYs, please report to the Principal’s office to be scheduled for ‘Remedial Econ 101.’ Apparently you were not paying attention. It is not ‘Advanced Economics’ that there are many, many factors besides the simple principle of ‘supply-and-demand.’ Also, we have some folks here who would like to speak with you about displacement of residents who live in neighborhoods of color. Please report immediately, before getting on Twitter with more of your ignorant blathering.”

Anybody ever tell you about how hard it is to read sans serif text? There’s a good reason all novels and newspapers have serif text – it doesn’t tire the reader’s eyes. Thank you.

We have all heard the argument that the housing market is segmented, it was argued that we could not experience a national housing crisis for that very reason, and then we witnessed exactly that, a national housing crisis that brought down the rest of the national economy.

This was a great article. One point I would have liked to see addressed is the fact that so-called ‘middle income’ is not calculated very fairly, especially here in the Bay Area. The income of Google, FB and Youtube employees is so much higher than what anyone else is earning, ‘middle’ is quite relative. The bottom line is that if everyone is priced out of living here, there will be nobody left to make those posh pumpkin spice lattes.

If cities don’t allow new “luxury” housing to be built, then middle cost housing will become high-cost and high-cost housing will become luxury.

Suppressing market-rate housing leads to gentrification.

Filtering has come in for a load of ridicule but it does work to some degree. Or it did…

I don’t see how filtering is going to work where most new construction is high-rise.

Public opinion is much smarter than the authors of this article and those conducting the survey.

More affordable housing for elderly & disabled on social security is the solution, after all these years of dishonest cost of living adjustments have left them living on a third of the poverty rate.

Here in Metro-Denver we have been building new housing as fast as we can possibly build it for most of the last 30 years and today our median home price is 425% higher than in 1990. Even today with an out of control pandemic there are more than 600 new mainly single-family subdivisions under construction on our suburban fringe with hundreds of infill and scrape and replace projects going in both our city and inner suburbs. Huge old shopping malls have been demolished and have replaced by multi-story new towns, and still our median home price is up by 60% since 2013.

Who wants to see home prices fall? Anyone who already owns a house? No. Anyone who owns an apartment building? How about someone who owns 50 or 100 or 5000 apartment complexes? No. Here it is quite common for a developer to buy an older single in the city and scrape it, then replace it with 2-4 units, that cost 50%-more to double what the original house was worth. How is that making housing more-affordable? All it is doing is running lower-income residents out of town.

You want affordable housing? Check-out Betenbough Homes in Amarillo, TX. They have several subdivisions there with brand-new singles from $131K and up, in-fact they have more than 20 different models between $131K and $179K base price. Sure, land is cheaper in Amarillo but not by a tremendous amount. How can they build the same house that costs $400K here and over $1 million on the west side of SF Bay for under $150K?

I blame free market neoliberalism. In the 1960s and 1970s just about everywhere in America has a viable local economy. There wasn’t a huge amount of difference in home prices. In 1970 the median home price in San Francisco was only 24% higher than the median home price in Detroit. Both cities are and were Democrat strongholds.

As of a year ago, before COVID, the median home price in San Francisco had risen to 38 times that of Detroit. Before free market neoliberalism it was rare for a city or town to see its economy destroyed. Now it is fairly common. Mass consolidation, offshoring of production, robotics. You want to see home prices and rents fall? Just kill the local economy. I have seen home prices fall by 80% in an urban area of 5 million people in my life. You couldn’t give houses or apartments away. In-fact just 9 years ago just inside Detroit’s city limits there were over 70,000 abandoned houses. What is so great about losing everything you own?

When my wife and I own a $650K house that our entire life savings is in why oh why would we want to see its price fall? We have worked for 33 years to build-up enough home equity to retire on. Even our three Millennial-age sons own their first houses now too and they don’t want to see their investment fall in price either.

We used to have lots of affordable housing in America but warehousing too many poor people too close together had a number of negative side-effects. Just about everywhere public housing was built the long-term effect drove jobs out of the surrounding area. Fear of our previous mistakes with public housing is one of many reasons current homeowners want nothing to do with affordable housing.

There is plenty of affordable housing in America thanks to neoliberalism, just none where wages are well above-average. My wife and I have worked our way up for 45 years since leaving high school. Why would we want to see our home price fall or our equity and quality of life it took decades to build-up lost? That’s the way I feel. What is so wrong with having to work your way up? If you can’t afford the Bay Area there are plenty of places you can afford to live.

It isn’t the public that needs to learn more about economics, it’s “professional” city and state planners that have been suckered into the so-called “Middle Housing” / “Trickle-Down” / “Filtering” religious cult. Oh, and if you try to provide evidence-based arguments, you’re doing nothing more than protecting your elitist, racist, white privilege. (No matter that many savvy “just housing” advocates who loathe the YIMBYs are non-White.)

This is a good article, but has a couple of unfortunate flaws. First, far too slanted references (12) to “experts,” e.g.

“Dillon sought comments from experts who struggled to explain the results; they all agreed that the lack of supply is at the root of the problem. … I generally believe the experts.”

Scott Wiener has received massive donations from the rapacious private equity firm, Blackstone Group, who are rabidly pushing deregulation and the securitization of single-family homes as rental assets.

In fact, I’ve done a deep literature review, and the reliable research and not slanted analysis is overwhelmingly that deregulation of (nominally) single-family areas (e.g., to allow 3, 4, 6 dwellings where previously the limit was 1 or 2) and leaving the decisions of what gets built where and at what market price (typically rental) DOES NOT significantly improve the number of dwellings that are “affordable” (e.g., using the “30% rule”) to households that are “housing-cost burdened.” (Nationally, and in many city’s 90% or more if the households that are truly “housing-cost burdened” are “Low-Income” (e.g., 80% of Median Family Income).

The article does a good job of introducing Economics 103 (not “advanced” by any means). However, it doesn’t adequately drive a stake through the false claims of “Trickle-Down” and “Filtering.” (The article seems to conflate the two to a degree.”

While the article address why the range of price impact diminishes across price categories, it leaves out a critical element of “market-rate” housing policies — where sufficient demand is maintained (e.g., in Portland, Oregon where Californians have moved after selling million+ ranch housing in the Bay Area), developers will seek the highest ROI for the lowest risk, which is in the higher (no necessarily “Luxury”) range. Thus, the price “distance” between what’s built and even “mid-income” housing is so large that there is no significant “Trickle Down.” to benefit low-income housing. Also not emphasized is that there is a “virtuous” “Trickle Up” effect when housing is built that reduces the deficit of housing that’s affordable to low-income households, and the benefit accrues to “middle-income” households.

“Filtering” of supply is a factor in some case. However, even when it occurs — and in the right direction — it’s glacially slow and doesn’t accrue much benefit to lower income households until an area has had such extreme disinvestment as to become a highly undesirable area in which to live (e.g., because of crime, pollution, bad schools, etc.)

The article completely overlooks the rampant “filtering” in the other direction which is removing tens (or more) thousands of single-family homes from “affordable” rents. Blackstone and other private equity firms have bought up hundreds of thousands of distressed rental single-family homes. An explicit strategy is to “upgrade” rental houses and increase the rent. Blackstone, of course, touts this as “improving” and areas housing, which in some cases it is. But is inarguably reduces “affordable” housing. If you look more closely, Blackstone’s actions are not so benign. Recently, they halted their improvement of the “Stuvy” public housing when the City adopted regulations reducing Blackstone’s ability to convert rent-controlled dwellings to market-rate.

Further, “middle housing” is simply a category of housing forms that have no inherent benefit or harm. My wife live in a 1927 “2-over-2” quadplex of 1-bedroom units on an adequately-sized lot and a reasonable rent for a grad student at the time. But the latest example, just a few blocks away was scraping two low-cost, small, older homes (total of six bedrooms) and replaced with a 3-story quadplex with each unit renting at an astronomical rent of $3,600. Using HUD figures, this meant that two dwellings affordable to a family of 4 or 5 were removed from inventory.

Finally, the article didn’t emphasize that in “ripe” areas — e.g., lower cost, non-white (nominally) “single-family” neighborhoods that are close to amenities and have been upzoned, private equity firms are buying up rentals that have a low structure-to-land ratio to scrape and redevelop at much higher rental rates. This leads to well-documented “direct” displacement (demolition) and “indirect” displacement (higher rents on existing houses) because of the “gentrification.”

The fundamental premise of this article is wrong and no amount of deep diving into details or pseudo-academic theories can correct that. In the SF Bay Area we have the most expensive housing in the U.S. It is because of supply and demand. This is one of the most desirable places to live — in the world. San Diego and LA are slightly less expensive but the dynamics are the same. The notion that when a new unit is built, someone from the area moves in and that creates a vacancy where they were, is not valid. Some of the demand is from people with money moving from abroad. Some is from young people from all over the US because California is still a magnet. Some is from people relocating from other states because the CA economy continues to generate good jobs.

The result is that demand overwhelms supply. Even a major increase in housing units will not result in a major decrease in housing prices. The truth is we do not have a housing crisis here. We have an affordability crisis. That is a crucial distinction.

It is folly to believe we can build our way to affordability. That’s like the folks in LA who thought they could eliminate the traffic problems if they could build enough freeways.

At a more micro level, the paper’s reliance on “trickle-down housing” is at least as compelling as Reagan’s reliance on “trickle-down economics”.