This article is part of the Under the Lens series

Discrimination in the Marketing & Maintenance of REO Properties

This post, submitted by the National Low Income Housing Coalition, is part of an ongoing series based on the National Fair Housing Alliance report, “The Banks Are Back, Our Neighborhoods Are Not,” that examines ongoing discrimination in the marketing and maintenance of bank-owned foreclosed properties.

This post, and the entire series, is also posted on Race-Talk, a blog hosted by the Kirwan Institute for the Study of Race and Ethnicity.

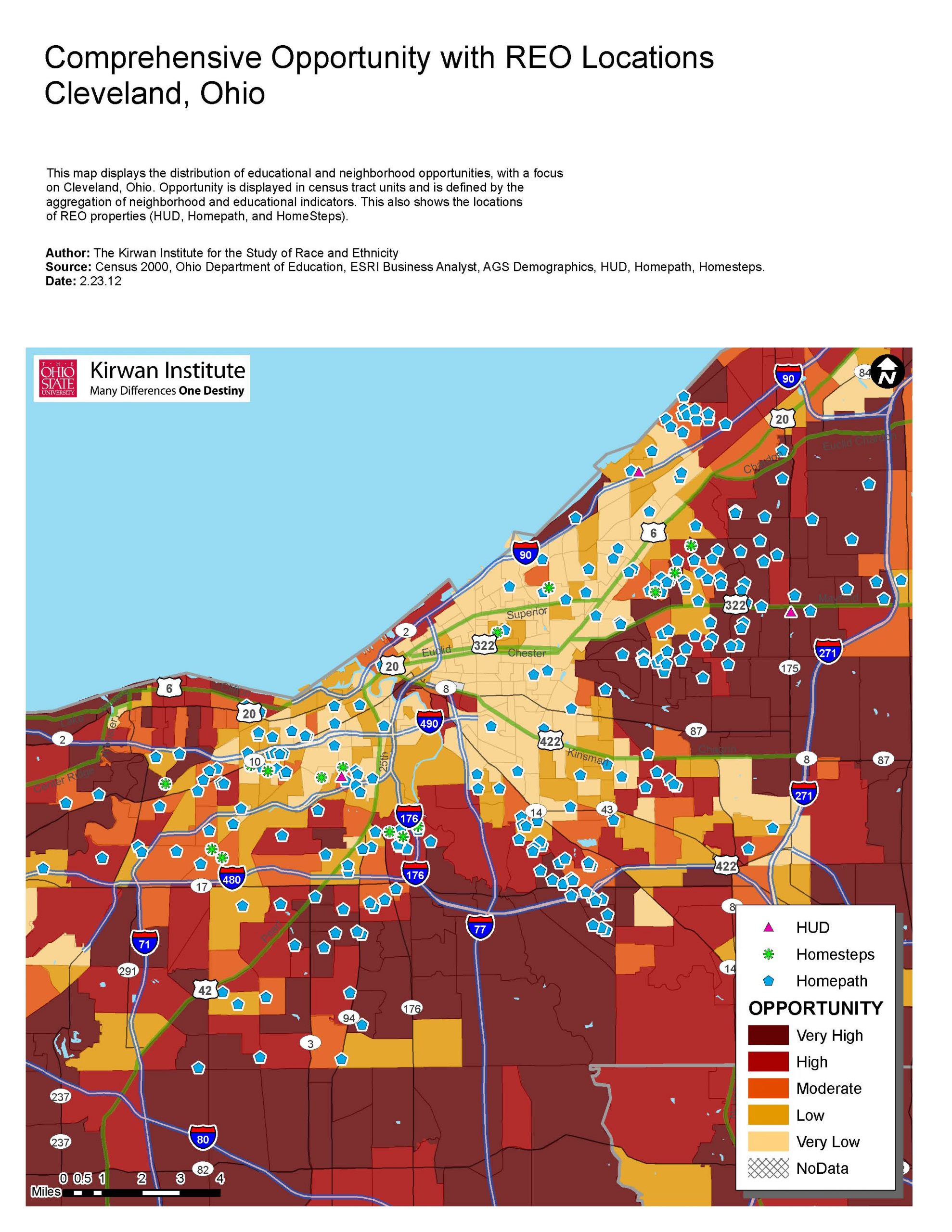

The National Fair Housing Alliance’s report, The Banks Are Back, Our Neighborhoods Are Not: Discrimination in the Maintenance and Marketing of REO Properties, has people talking over at the National Low Income Housing Coalition. It’s not just the report’s finding that bank or “real estate-owned” (REO) properties in white neighborhoods are much better maintained and marketed by private than such properties in African-American and Latino neighborhoods. It’s what the report’s findings might mean for the REO-to-rental pilot program launched by the Federal Housing Finance Agency (FHFA) in late February.

There are some differences. The report focused on REO properties held by private banks, while the properties included in the pilot are all held by Fannie Mae. Nonetheless, we at NLIHC see some lessons that can be transferred and that warrant additional attention, most notably the statement in the report that “banks have an obligation to implement sound quality control practices to guarantee REOs are maintained and marketed without regard to the racial or ethnic composition of the neighborhoods in which REOs are located.” NFHA also notes that “direct contracts with local vendors typically have better onsite maintenance of REOs.

NLIHC submitted comments to FHFA when the agency was seeking input on what an REO disposition program should look like, that include these general principles. Specifically, NLIHC emphasized that community-based and mission-driven organizations with strong track records should be given the opportunity to participate in the program, to ensure proper maintenance of rental properties. NLIHC also noted that past efforts to dispose of REO properties held by FHA have not been as successful as they could have been because there was no associated funding provided to help with operating and rehabilitation costs. We recommended that REO sales be paired with National Housing Trust Fund dollars to make some of the properties affordable to extremely low income households. Finally, we recommended that landlords and property managers must contractually agree to meet certain housing quality standards for all properties, whether or not a particular unit is subsidized.

The first FHFA pilot includes few restrictions, none of which relate to affordability. However, it is extremely small scale, with fewer than 3,000 properties included, the majority of which are already occupied. FHFA has indicated that this pilot is just the first step in a REO disposition program. It is important that advocates weigh in now to ensure affordability, maintenance, and marketing issues are all sufficiently addressed as the REO-to-rental program takes shape.

What do you think? Do you see ways that affordability and adequate maintenance can be woven into future iterations of the REO-to-rental program? Let’s talk about it in the comments.

What do you think? Do you see ways that affordability and adequate maintenance can be woven into future iterations of the REO to rental program? Let’s talk about it in the comments.

Comments