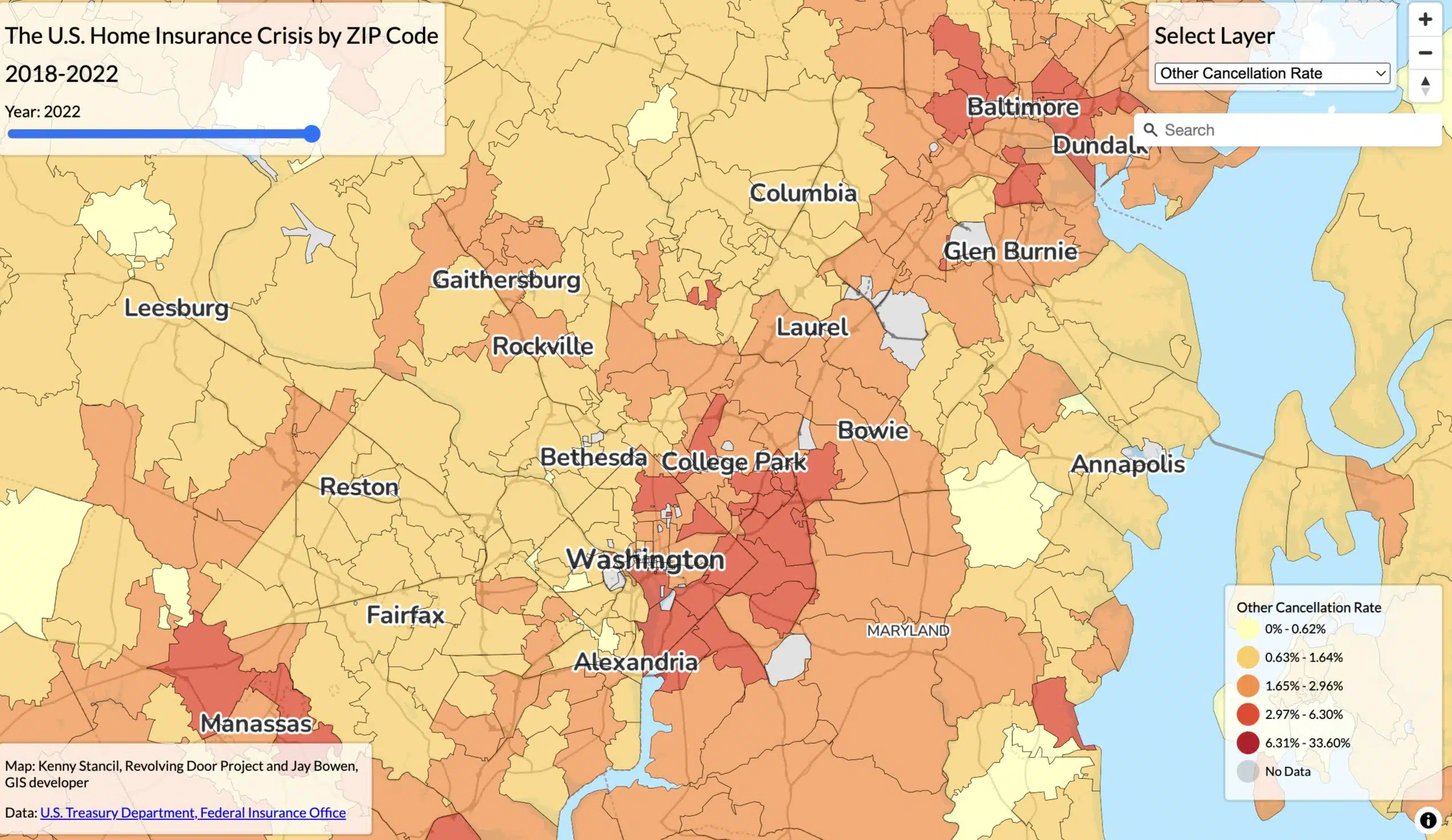

Escalating climate risks and natural disasters, as well as insurance companies’ opportunism, are causing upheaval in the homeowners’ insurance market, leading to a crisis in availability and affordability, and a new wave of exclusion called “bluelining.” That’s when financial institutions like banks, credit facilities, and insurance companies steeply increase prices or withdraw services from communities that have high levels of environmental risk.

Unlike historical redlining, where lenders denied financial services to people who lived in predominately Black neighborhoods, the geographic exclusion of bluelining is not directly based on race. However, bluelining is often happening in the footprints of redlining. If left unchecked, it could replicate old patterns of disinvestment and decline in communities that already are most socially vulnerable and have limited resources to cope with ever-increasing disasters like fires, flooding, and other extreme weather.

At the Consumer Federation of America and The Greenlining Institute, we have worked for decades to improve oversight of financial institutions like insurance companies, and mitigate the harms caused by redlining. We are sounding the alarm on this new frontier of climate-driven financial exclusion and offering a few policy tools to better respond to it.

The Emergence of Bluelining

People who live in formerly redlined neighborhoods are disproportionately Black and Hispanic. Because of decades-long inequitable access to capital and resources, many redlined communities also have an older, more vulnerable housing stock, and greater exposure to environmental and natural disaster risk. These formerly redlined neighborhoods face higher climate risk due to proximity to hazardous industrial sites, less tree canopy, and an overall underinvestment from both public and private actors in resilient infrastructure, leaving them especially vulnerable to climate-driven financial discrimination.

As a result, bluelining has the potential to exacerbate disinvestment. It leaves communities that have long been denied adequate investment—communities that are now bearing the brunt of climate impacts—without the financial resources to withstand and recover from storms and other weather-related events.

Insurance companies are at the forefront of bluelining today, effectively making determinations about which communities remain insurable and have a future and which communities will not. Without insurance, it is impossible to get a mortgage, and when people can’t get mortgages, the value of homes in that neighborhood plummet.

But bluelining also has implications beyond the availability of property insurance. When insurance coverage is insufficient, mortgage lenders and securitizers—notably Ginnie Mae, Fannie Mae, and Freddie Mac, which hold the credit risk of most U.S. mortgages—are exposed. And while insurance companies may be the first to begin withdrawing from climate-vulnerable areas, other financial institutions are starting to follow in deciding where to originate a mortgage or loan, and at what price.

This risk is finally being recognized at the highest levels. In February, Federal Reserve Chairman Jerome Powell testified in front of the Senate banking committee in reference to high-risk communities. “If you fast forward 10 or 15 years, there are going to be regions of the country where you can’t get a mortgage. There won’t be ATMs. You know, the banks won’t have branches and things like that,” Powell said.

As insurance companies and lenders increasingly factor climate risk into their business strategies, communities may witness a resurgence of racial and economic exclusion that mimics redlining practices. And as this financial and climate ripple effect intensifies, we may see a new cycle of neighborhood decline.

How Bluelining Will Shape Neighborhood Decline

Bluelining not only makes it hard for individual households to get insurance; it affects entire communities. In the highest-risk communities with the most expensive insurance premiums and lowest level of insurance availability, more and more homeowners are going underinsured and uninsured. An analysis of 2021 American Housing Survey data from the US Census Bureau shows that 1 in 13 homeowners in the United States are uninsured. Homeowners of color are disproportionately at risk.

Those without insurance are at risk of losing their homes and possessions in just one storm or disaster. Over time, this means that neighborhoods with many uninsured homes will have more vacant housing or housing in disrepair. The lessons from depopulated cities show us that this vacancy often leads to a downward spiral in surrounding property value and undermines the local tax base. As a 1968 Congressional report concluded, “Communities without insurance are communities without hope.”

When companies blueline communities and restrict access to insurance and mortgages, more residents and businesses may be forced to leave, accelerating a cycle of depopulation. While the last century saw suburbanization, this one may be defined by climate migration, as people flee vulnerable areas for safer ground. Amid this mass exit, the families left behind will be those with the fewest financial resources to move. They’ll be forced to live with crumbling infrastructure and dwindling support.

Without proactive, equitable climate and insurance policy, these trends could mirror and extend the legacies of redlining—deepening racial and economic disparities.

Fighting Back

If these trends become the norm, the challenges of housing disinvestment, shrinking tax bases, and unavailability of financial services are likely to reemerge in climate-impacted places. To prevent this, policymakers must ensure that communities, especially historically marginalized communities, are not left without protection, resources, or a voice in shaping their futures.

As history risks repeating itself, we can start to meet this moment by retooling policies first developed in response to redlining and apply them to the insurance industry.

First, insurance companies should be required to annually disclose their pricing, underwriting, denials, and claim payouts in every census tract, akin to what the Home Mortgage Disclosure Act requires financial institutions to do. There is a severe lack of publicly available data on insurance access and pricing. While laudable efforts in the recent past by the Federal Insurance Office and the Senate Banking, Housing, and Urban Affairs Committee have aimed to close this gap, they have not led to consistent and robust transparency into property insurance.

By contrast, to prevent redlining, since 1975 mortgage lenders have been required to annually disclose data on every mortgage application they receive. This has provided critical transparency and accountability of the mortgage industry and allowed regulators and the public to detect potential discrimination before it takes hold. As homeowners’ insurance increasingly determines who can own a home and where, insurers should be required to report homeowners’ insurance data in the same manner as mortgage lenders. Such transparency can help prevent unfair discrimination in pricing and access, both between different communities and within communities, where it is targeted at the most vulnerable homeowners. State insurance commissioners should work alongside the Federal Insurance Office to enforce and coordinate this data collection and distribution.

Second, lawmakers should pass state-level community reinvestment acts to require insurance companies to invest in climate risk reduction and resiliency. Examples like California’s Organized Investment Network and the 25-year-old Massachusetts Insurance Company Community Investment Initiative offer voluntary frameworks for directing insurer investments into environmental, housing, and other underfunded needs.

States should launch these kinds of initiatives to ensure that insurance companies become partners in reducing risk and safeguarding communities, rather than only being in the business of profiting from risk. Indeed, insurance companies have extensive investment portfolios, which are a key contributor to their financial bottom line, but many of their investments are exacerbating climate change and driving up costs for communities and homeowners. It is time for insurance companies to become part of the solution rather than part of the problem. With appropriate oversight, state-level community reinvestment acts can drive much-needed investment dollars into resilient communities and housing, while helping lower overall risk and ultimately, the premiums homeowners must pay.

As we foresee a new cycle of neighborhood decline driven by bluelining, we must apply time-proven policy tools to insurance companies. Insurance companies must be held accountable to where and with whom they do business—their decisions increasingly drive the future of homeowners and communities—and must also become investment partners in risk reduction. To prevent bluelining, transparency and investment are critical first steps.

Preventing disinvestment in declining neighborhoods is a worthy objective, but, this monitoring must be combined with pro-active efforts to address the abject failure of “economic development” efforts which perpetuate our socioeconomic disparities. Such large subsidies to the private sector at all levels of govt for decades has only sustained a class divide; many “people of color” who serve in these capacities in regulatory and policy circles say nothing and do nothing about this structural reality. I have pointed out this problem for a long time, but there is no interest to address this longstanding problem. I’m asking for transparency and accountability similar to what Sharon and Monica are asking for in their capacity.