This article is part of the Under the Lens series

This article was originally published by NPQ online, Feb. 2, 2022, and is used with permission.

I work and live in California, the poster child of the national housing crisis. Here the median home price is $800,000, but prices are much higher in coastal metropolitan areas, with the median home price in the San Francisco Bay Area reportedly nearing $1.3 million. The poverty rate is the highest in the nation when housing is considered. Not surprisingly, homelessness is skyrocketing. Prices are surging everywhere in the country. U.S. home prices surged 18.4 percent in November 2021 from a year earlier. About one quarter of renter households are spending more than half of their income on rent.

The prevailing narrative, especially in California, explains the high cost of housing as resulting from a lack of supply due to local government and NIMBY (Not in My Back Yard) opposition to new development. While such NIMBYism is certainly a factor, it is surprising that similar attention is not being paid to other underlying causes, including restrictions on development in undeveloped areas, higher labor and land costs, and the global flow of investments. Most surprising is the lack of attention on the Federal Reserve, even though its policy interventions have had profound effects on housing prices.

the great experiment

The Great Recession of 2008-09 was the second-worst economic crisis in U.S. history, after the Great Depression. In response, the Federal Reserve engaged in a “Great Experiment,” the wide-scale purchasing of bonds—especially mortgage-backed securities—to the tune of $120 billion a month. Such a huge injection of money into the economy is known as Quantitative Easing, or QE. The Fed hoped that, together with bringing down interest rates to practically zero, QE would save the economy.

It worked—to a point. As shown in Frontline’s “The Power of the Fed” episode, it was hoped that access to easy money would prompt corporations to invest in productive capacity and create more jobs. Instead, companies engaged in a huge buyback of their stock, propelling the stock market to new highs. The share of the financial sector in gross domestic product (GDP) grew sharply.

While Wall Street thrived, millions of people lost their homes because of their inability to pay mortgages—mortgages that had been foisted on them in large part by banks and mortgage companies. It has been calculated that in the crisis Latinx and Black Americans collectively lost half of their collective wealth. The federal government did not help them, but heaped benefits on Wall Street and the financial sector, widening the inequality gap even further.

In 2013, in response to the Fed’s surprise announcement of a reduction in QE (dubbed “tapering”), Wall Street induced a mini-panic in global markets—what has been referred to as the “Taper Tantrum.” As a child responds with a tantrum to the withholding of candy, so did the market respond with a crash. The Fed quickly recanted. Only in 2014 was the Fed able to end QE without a tantrum, by promising to keep short-term interest rates low.

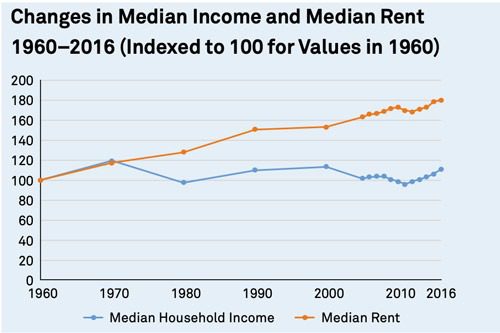

By 2018, housing prices had recovered from their Great Recession losses and recommenced their inexorable increase. Until the 1970s, housing costs and wages had increased at roughly the same rate. Beginning in the early 1970s, however, wages and housing costs started to diverge, with the gap widening over time. This divergence is the basic reason for the housing crisis.

covid-19: the great experiment revived

As a result of COVID-19, the Fed restarted QE in March 2020, once again at a rate of $120 billion a month—and lowered interest rates to near zero. A year later, the economy seemed to have recovered, not so much due to the Fed’s action but because of the relief bills passed by Congress. Again, the benefits accrued disproportionally to the rich. As Karen Petrou, the author of Engine of Inequality: The Fed and the Future of Wealth in America, published in 2021, observed: “The benefits of the Fed’s huge QE-based portfolio . . . over time were 10 times greater for stock market prices than for overall economic prosperity.” Addressing how QE and extremely low interest rates affect housing prices, Petrou explained that “low interest rates set by the Fed spur lending, creating more demand to purchase homes and forcing prices higher. Rising equity is great for existing homeowners, but richer Americans who own property are the ones who benefit the most.”

In fact, by late 2020 home prices had already started to soar, contradicting many experts’ predictions of a drop due to COVID-19. Several factors explain this upsurge, but the Fed definitely had a hand in it. In “Home Prices Are Roaring. Is That the Fed’s Problem?,” Jeanna Smaller, a New York Times reporter, wrote that, “some fret that the central bank’s big bond purchases could be helping to inflate . . . the housing boom.”

Pouring easy money into the economy has heightened the search of capital for assets to invest in, and housing is an obvious target. The financial sector—the REITs (real estate investment trusts) and the BlackRocks of this world—has been pouring money into housing for decades, but a buying frenzy has captured small speculators as well. On Nov. 21, 2021, a report came out declaring that “Investors are 51 percent of Southern California’s home buying surge.” In “Madhouse,” an article in the New York Times Magazine, Francesca Marti, a frequent writer on housing and inequality, pointed out how “[i]n Austin and cities around the country, the crazy real estate market has forced regular people to act like speculators.” In December 2021, the Fed announced that it would act more quickly on tapering its quantitative easing. That, however, was not about the red-hot housing market, but rather due to its concern about persistent and growing inflation.

how quantitative easing affects housing inequality

The Federal Reserve’s dual mandate is to maintain full employment (so people who want to work can find employment) and price stability (an inflation rate of around 2 percent). Traditionally, the tool the Fed has used to try to keep the two in balance—a difficult proposition—is interest rates. Increasing interest rates is utilized when inflation threatens, as is happening now. Lowering interest rates makes borrowing easier for business to expand or families to get mortgages, helping the economy grow, and that is exactly what the Fed did in 2010 and 2020, when Fed officials lowered the prime rate—the rate at which money is lent to the banks—to near zero. An aside: The banks get the money basically for free from the Fed and lend the money back at higher interest rates. The Fed, then, “is simply giving them a hidden gift worth billions and billions of dollars,” as Nobel Prize-winning economist Joseph Stiglitz explained in his 2013 book, The Price of Inequality.

But in 2010 and 2020, the Fed added a new tool, quantitative easing. By buying bonds and other assets from banks and other financial institutions, the Fed made sure that they had cash, plenty of it, to lend out. According to Petrou, through this largesse, the U.S. became after the Great Recession, “far more unequal far faster.” The COVID-related second round of free money doubled down on this trend—for example, the Standard & Poor’s 500 stock index doubled its value from March 23, 2020 (its pandemic low) to Aug. 16, 2021, but QE has benefited the great majority of people far less. As Stiglitz put it when writing about the Great Recession, “the Fed in its policies has often seemed oblivious to the distributional implications of its decisions.”

Housing is a key player in the dynamics of inequality. The combination of rock-bottom interest rates and abundant cash-seeking investment opportunities has spurred a huge demand for housing, even as supply has remained the same. The inevitable result is a red-hot housing market.

Soaring housing prices have a dual effect on inequality. On one hand, they increase the wealth of homeowners (and eventually their children). On the other, through rising rents, they make poorer the increasing number of people who cannot afford to buy a home (and eventually their children). Asset inflation, already underway since the 1970s because of the Fed interventions in 2010 and 2020, has become magnified and entrenched.

Housing is not the only mechanism through which wealth becomes concentrated at the top. So does the stock market. But housing is fundamental to the distribution of wealth. According to Australian sociologists Lisa Adkins, Melinda Cooper, and Martijns Konings (2021), access or lack of access to housing ownership has become the new class divide of the 21st century. They propose five main classes: investors, outright homeowners, homeowners with mortgages, renters, and the homeless. This proposed class scheme provides new lenses to examine frictions between generations, as between the home-rich boomers and the already debt-weighted millennials.

If high home prices and rents are hallmarks of inequality, the actions of the Federal Reserve should give us pause. Granted, the crises did call for Fed intervention. What is inexcusable is that when by spring 2021 it became clear that the economy was recovering and housing prices were skyrocketing, they held off on tapering QE and gradually increasing interest rates. Why? One likely explanation is the Fed’s subservience to the financial sector and fear of another “taper tantrum.”

The two economic crises have not been unique to the U.S., but have been global, including G-7 nations and additional countries such as Australia and New Zealand. These countries have resorted to similar policies. And in those countries, too, central banks privileged the interests of the financial sector, disregarding the impact of their policies on the larger economy. Housing prices have soared globally as well.

But in New Zealand something unusual happened. In February 2021, the government of Prime Minister Jacinda Ardern sent a letter to the central bank requesting that it consider the impact that its monetary policy decisions have on housing prices to help calm the country’s property market. In the U.S., President Joe Biden does not seem to be too concerned about the supercharged housing market and its role in worsening inequality. In fact, Biden nominated Jerome H. Powell for a second term.

We need a much larger debate about the proper role of central banks in an age of widening inequality. In New Zealand, the government—by asking the country’s central bank to take housing affordability into consideration when establishing policy—broke the taboo against political interference in central banks. Maybe we should ask for more. As Petrou observes in her book, “Instead of regretting inequality even as it makes inequality worse, the Fed can and must quickly rewrite policy with a new goal in mind: shared prosperity.” Access to housing, of course, is fundamental to achieving a more economically just society.

I don’t get how this is supposed to be so important or how it explains a pre-existing trend going back to 2000. If interest rates were raised, all things being equal, home-building should have been reduced, not remained constant. The obvious conclusion is that all things aren’t equal. If prices keep going up, what is the mechanism to stop more supply from happening?

Excellent article and right on the point. You must be doing good work because I seen a while back at president did have a meeting with the head of the Fed and after that meeting the Fed started raising interest rates and started quantitative tightening.

Just like that comedian always said, it’s a big club and you ain’t in it. The people who are renting or looking for a house have been decimated by the FED policies.

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered.” – Thomas Jefferson

Some people say this quote is not real but it is just amazing how it’s come to fruition. Look at all the homeless it’s so sad what’s happening in this country the corruption at the top.