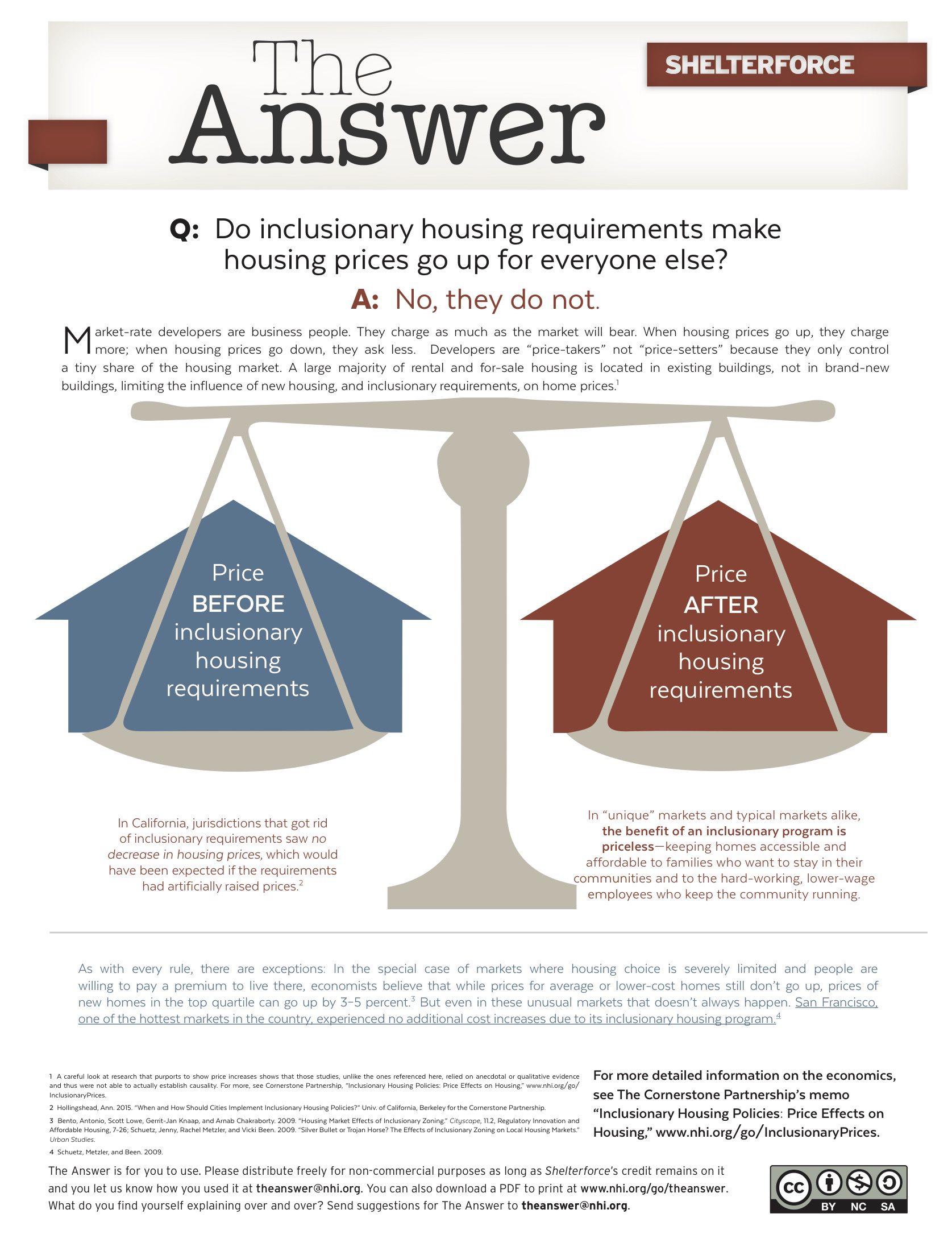

Courtesy: NYC Neighborhoods

As communities and government leaders prepare for rising sea levels and more extreme weather, including major floods, it is essential that our policy response promotes social equity and increased resilience at both the household and community levels. Unfortunately, with federal flood insurance reform, we are seeing the opposite impact. Rising flood insurance rates are threatening the ability of the homeowners we work with at the Center for NYC Neighborhoods to remain in their homes and neighborhoods. Caught between extremely costly retrofitting measures or soaring insurance rates, these low- and moderate-income families are at grave risk of financial instability, foreclosure, or even displacement.

The massive destruction caused by Hurricane Sandy forced New Yorkers to contend with the reality of the city’s vulnerability to rising sea levels and increasingly extreme weather. Sandy’s damage was immense: 44 New York City residents lost their lives, 17 percent of the city was flooded, and nearly 90,000 buildings were damaged. The disparities among those most affected by the storm were also significant. While some wealthier enclaves were hit by the storm, most of Sandy’s victims were public housing residents and low- to moderate-income homeowners.

New York’s experience with Sandy is hardly unique: it is well-known both nationally and internationally that natural disasters disproportionately harm lower-income households. At the Center for NYC Neighborhoods, we work with homeowners in neighborhoods like Canarsie in Brooklyn and the Far Rockaways in Queens that are home to middle- and working-class families still recovering from the storm. These neighborhoods were already hard-hit by the foreclosure crisis when Sandy struck, not to mention the legacies of redlining, disinvestment, urban renewal, and planned shrinkage. Now they are being disproportionately affected not only by the storm itself, but by measures being put in place to prepare for the next one.

How Did We Get Here?

New York City’s flood-prone neighborhoods are, for better or worse, among the last bastions of so-called “naturally occurring” affordable housing in a famously high-cost city. Deliberate policy choices led to the location of so much lower-cost housing within them, which decision makers should remember when deciding how much of the cost of flood protection those residents should bear.

For most of its existence, much of New York’s 520-mile waterfront was industrial, and largely used for the production, warehousing, and distribution of goods. After World War II, Robert Moses built over 400 miles of highway in the region, much of it lining the city’s waterfront. While his plans raised land values in the city as a whole, it drove them down in coastal neighborhoods, which were beset by noise and smog.

Around the same time, an unprecedented wave of homeownership began. The Federal Housing Administration (FHA), alongside other government-backed and private-sector lenders, made homeownership more affordable as returning soldiers settled down and started families. Not all neighborhoods, however, were eligible for FHA loans. An agency called the Home Owners Loan Corporation (HOLC) evaluated various neighborhoods to judge how safe they were for investment. The HOLC was notoriously racist and xenophobic, and, as a result, they graded neighborhoods with almost any immigrant or African-American presence as unsafe. The HOLC downgraded Brooklyn’s Manhattan Beach, for example, because its surveyors found a “slow infiltration of somewhat poorer class Jewish” residents; they derided Lower Bath Beach for its “low grade Italian population.” No neighborhood with any African American population received a grade over B-. Many neighborhoods were cut off from home loans and fell into disrepair.

In the post–World War II era, New York City began experimenting with “urban renewal” planning. Shoreline neighborhoods became urban renewal targets for three main reasons: they were where poor people already lived, their land was relatively easy to acquire due to its low value, and, in a self-perpetuating cycle, their land was often near other projects. And so, many of these neighborhoods became home to high-rise housing, hospitals, mental health facilities, and nursing homes. While some of those developments constituted a public good, the surrounding land values dropped further as a result of their presence.

Urban renewal was not only traumatic for the people it displaced and the neighborhoods it disrupted, it was also extremely expensive. In the 1970s, the federal government stopped funding urban renewal projects as New York City plunged into a fiscal crisis. In the immediate aftermath of that crisis, the city’s approach to its working-class neighborhoods was crystallized in a phrase coined by Housing Commissioner Roger Starr: “planned shrinkage.” Under this approach, the city focused its constrained resources on the central city and aimed to retain the rich. The city’s poorer and more distant neighborhoods, including most of its waterfront, saw a decline in city services. Vacancies rose, fires tore through neighborhoods, and waterfront land values continued to drop.

A few years later, the city, under Mayor Ed Koch, partnered with community development corporations to restore and build new subsidized housing on publicly owned vacant lots and tax-foreclosed properties. Much of this work took place in today’s flood-prone shorefront, including the Rockaways, Jamaica, Sheepshead Bay, Throggs Neck, and Staten Island’s North Shore.

Though residential development along the waterfront did become geared toward high-income households in neighborhoods like Long Island City and Williamsburg, in many other areas, the waterfront remained a bastion of affordable homeownership, where communities live by choice and by chance amidst rising real estate pressures. The devastation of Hurricane Sandy highlighted this reality, but it also imperiled it. The cost of staying put is rising every day, and the flood insurance premium hikes now underway threaten the future of low- and moderate-income homeownership in these parts of New York City.

The Challenge: Rising Rates

Though most individual flood insurance policies are purchased through private insurers, nearly all of these policies are provided through the National Flood Insurance Program (NFIP), administered by FEMA. In an effort to make the program more financially sustainable after the losses incurred from Hurricane Katrina, Congress passed the Biggert-Waters Flood Insurance Act in 2012, followed in 2014 by the Homeowner Flood Insurance Affordability Act.

A major component of these reforms was to phase out subsidized rates that had been granted to properties built before a community joined the NFIP and adopted a flood map. For New York, this means all structures built before 1983—a startling 80 percent of properties in the floodplain. Because these properties were built before the city adopted NFIP floodplain management standards, they are, in large part, at a lower elevation than is required for post-1983 construction.

As a result of these reforms, flood insurance rates across the country are increasing significantly—and they are disproportionately hurting middle- and working-class households in dense, urban areas with older homes, like New York City, Newark, or Baltimore. Many homeowners are seeing their flood insurance rates rise by up to 18 percent every year. Others (including businesses and owners of homes with substantial or repetitive insurance losses) face even steeper rate increases of up to 25 percent when they renew their annual policy. For many, these costs will now rise every year due to changes in federal flood insurance regulations. Currently, homeowners generally pay between a few hundred and $2,000 a year. However, based on current rate calculations, some homeowners could ultimately expect to pay as much as $10,000 per year as the rates continue to increase.

What’s worse, many homeowners are left without options to mitigate their risk and lower their insurance rates. Currently, FEMA considers home elevation the only means for homeowners to lower their rates, even though other far less costly measures can dramatically lower the potential risks and related costs. In New York City, elevation on a widespread scale simply does not make sense: almost 40 percent of our buildings would be extremely challenging to lift because they are attached, semi-attached, or on lots too narrow to allow for elevation. For example, mechanical systems could be relocated from basements to attics, or applying techniques called wet or dry floodproofing would allow homeowners to either prevent water from entering their homes or allow it to enter in a controlled manner that avoids damage.

FEMA is in the process of updating New York City’s flood maps, which, when adopted, will vastly expand the portion of the city where homeowners are required to purchase flood insurance. If FEMA’s proposed maps for New York City are adopted in their current form, twice as many people will be designated as living in high-risk flood zones—totaling over 400,000. The final shape of the updated maps is yet to be determined, as the City of New York has filed an appeal with FEMA arguing that the map overestimates the size of the high-risk flood zone. Though this appeal will delay the its adoption, the new flood zones will undoubtedly be larger when the new maps are finalized.

Responding to the Challenge

Confronting the stark challenges posed by both rising tides and rising costs will require a concerted, long-term effort to arrive at solutions that protect communities in flood-prone areas. We propose the following recommendations to ensure that flood insurance reforms do not lead to the displacement of middle- and working-class families:

- Educate residents in flood-prone neighborhoods about their current flood risk, expected rate increases, and potential future risks caused by sea-level rise. Many homeowners remain unaware of, or confused by, both flood insurance rate increases and the floodplain expansion. We created FloodHelpNY.org, a user-friendly resource that allows homeowners to look up their address to find out if they might be affected by flood map changes and learn how they can prepare themselves.

- Ensure that FEMA develops alternative mitigation standards other than elevation for dense, urban neighborhoods with many attached buildings.

- Create a resiliency fund to provide financing for home elevations and other mitigation measures so that residents can both make their homes safer and keep insurance costs affordable.

- Explore new means-tested flood insurance subsidies for low- and moderate-income homeowners to replace the blanket subsidies that are currently being phased out.

- Continue to expand city and state buy-out and acquisition opportunities. When staying put does not make sense, homeowners often need financial assistance and concessions from mortgage holders to make relocation truly viable. Both New York City and New York state have begun voluntary buyout programs; however, the level of funding is not commensurate with the level of need and the programs require additional federal support.

While rising tides do not discriminate, their impacts on homeowners and their communities are not uniform. Across the country, those with lower incomes are more likely to live in more vulnerable areas, and those with less access to credit and savings have a much harder time rebounding from the effects of disasters like Sandy. If this challenge is not confronted head on, the safety, affordability, and stability of many of our neighborhoods, in New York City and beyond, are put at grave risk.

Comments