Row homes on St. Louis Avenue, city of St. Louis. Photo by Paul Sableman via flickr, CC BY 2.0.

Not long ago, I looked at a small neighborhood in northwest Detroit called Crary-St. Mary’s, named after the school and church that more or less bookend the neighborhood. In 1970 it was 98 percent white. By 1980 it was 84 percent Black, and by 1990 95 percent Black. By any other measure—household incomes, homeownership rates, vacancy rates, and family composition—it stayed pretty much the same. It went from being a solid but unpretentious middle-class white neighborhood to being a solid but unpretentious middle-class African-American neighborhood. It was one of many Detroit neighborhoods that went through that transition.

Almost every older city in America had one or more Crary-St. Mary’s, like Overbrook in Philadelphia or Baden in St. Louis. They weren’t paradise. The cities they were in were hurting, and over the next couple of decades they saw a lot of stresses. By the time the year 2000 rolled around, many of these Black middle neighborhoods were fraying around the edges. But most were still viable, functioning neighborhoods. They were places where families could thrive, and often the seedbeds from which generations of successful, strong African-American leaders sprang.

Around 2000, the cities themselves started to change in visible ways, and people started to publish books with titles like ‘comeback cities’ and ‘cities back from the edge.’ Cities like Baltimore and Pittsburgh started to grow jobs again, mostly in health care and higher education, which had replaced factories as these cities’ main economic engines. Thousands of young people with college degrees were flocking to the cities. In Center City Philadelphia and Baltimore’s Harbor East, developers were putting up expensive apartment buildings. Along St. Louis’ Washington Avenue, the old garment factories and warehouses were being turned into lofts and condos. “Gentrification” became the buzzword of the decade.

One might have thought that the cities’ revival would reinvigorate their Black middle neighborhoods, giving them the reinvestment shot in the arm they urgently needed. That didn’t happen. Since 2000, one African American middle neighborhood after another has lost ground, socially, economically, and in terms of the real estate market. Crary-St. Mary’s today is a high-poverty area, with boarded up houses on almost every block.

Not every neighborhood has declined. Some have continued to hang in, remaining fairly stable but challenged; a (very) tiny few may be showing signs of gentrification. But hundreds of neighborhoods, from Chicago to Philadelphia, St. Louis to Buffalo, are endangered, and thousands of African-American families are seeing their modest wealth disappear, and the quality of their lives deteriorate.

The picture is very different in the handful of “hot,” mainly coastal cities, like Washington or Seattle, where the influx of more affluent families and individuals is pushing up prices and exerting pressure on all neighborhoods across the city. But I want to concentrate on the larger number of other cities, mostly not on the coasts, including places like St. Louis, Baltimore, Chicago or Kansas City, cities with historically large African-American communities.

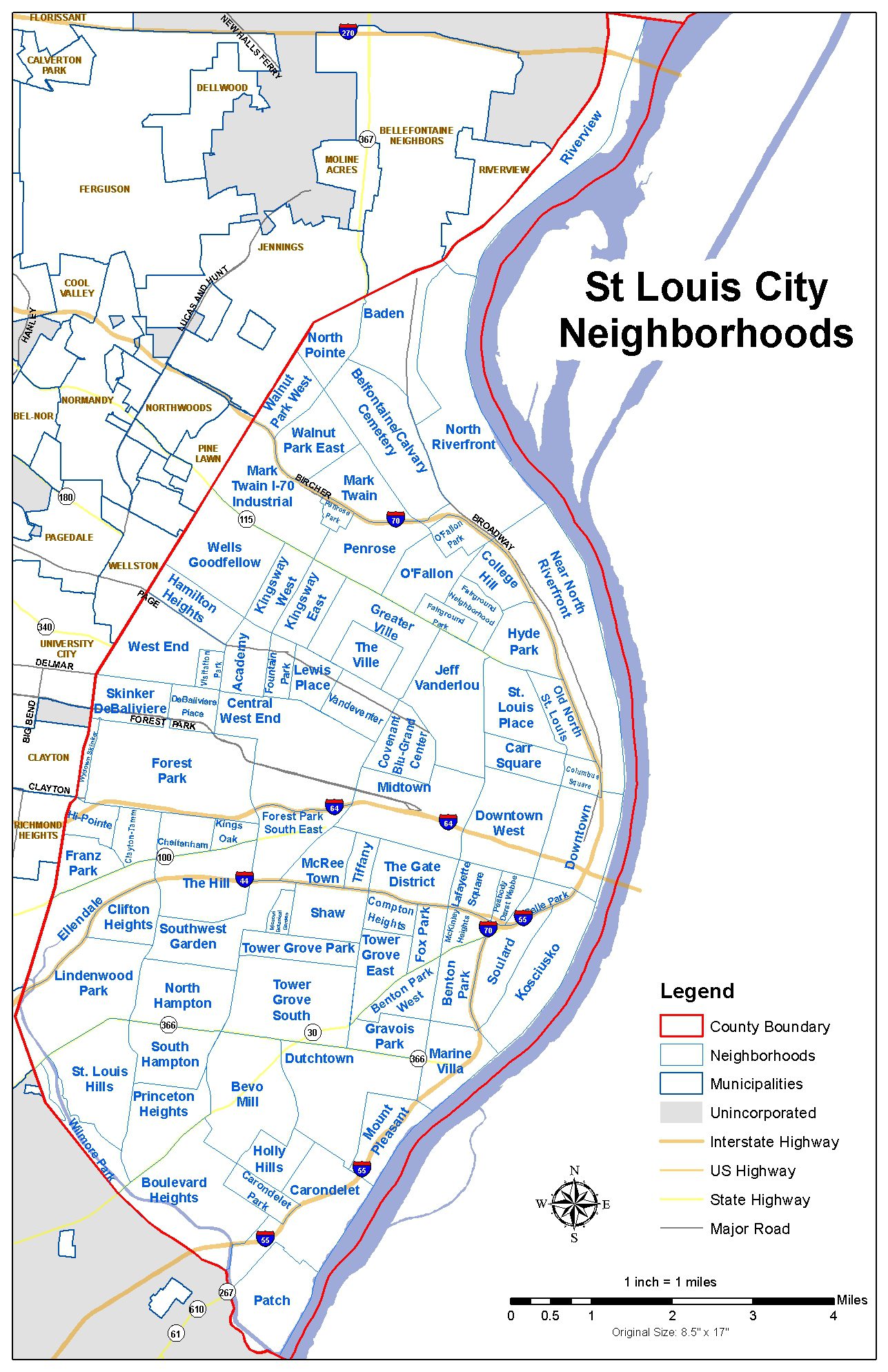

St. Louis: A ‘Middle of the Pack’ Older City

Shaped like a teardrop, St. Louis is a city of roughly 320,000, with a fairly even split of white and Black residents and small Latinx and Asian populations. The Mississippi River forms its eastern border. St. Louis’ Black population historically lived in Northside, north of Delmar Boulevard, a boundary known to generations of St. Louis residents as the “Delmar divide,” and south of Natural Bridge Road. South of Delmar is the roughly mile-wide Central Corridor, where downtown, the city’s major universities and medical centers, and its world-famous Forest Park, are found. South of the central corridor lies Southside, historically white except for a handful of Black enclaves, but today more than 25 percent Black.

Starting in the 1950s and 1960s, and accelerating in the 1970s, working- and middle-class Black families moved north of Natural Bridge Road, into neighborhoods like O’Fallon, Penrose, and Baden. These became the city’s Black “middle neighborhoods,” solid neighborhoods of single-family homes and homeowners. The neighborhoods, as Washington University’s Hank Webber describes them, “… the heart of American cities … the neighborhoods where working and middle class citizens live, raise families, pay taxes, send their children to school, go to church, synagogue or mosque, and shop at the local grocer.”

Starting in the 1950s and 1960s, and accelerating in the 1970s, working- and middle-class Black families moved north of Natural Bridge Road, into neighborhoods like O’Fallon, Penrose, and Baden. These became the city’s Black “middle neighborhoods,” solid neighborhoods of single-family homes and homeowners. The neighborhoods, as Washington University’s Hank Webber describes them, “… the heart of American cities … the neighborhoods where working and middle class citizens live, raise families, pay taxes, send their children to school, go to church, synagogue or mosque, and shop at the local grocer.”

In 2000, 18 St. Louis census tracts, mostly north of Natural Bridge Road, were African-American middle neighborhoods, with household incomes close to the citywide median; 60,000 people, or roughly one-third of the city’s Black population, lived in these neighborhoods. Many of these neighborhoods were facing challenges. Over the decades following 1970, most of the good manufacturing jobs that had moved many people into the middle class disappeared. Public services were often spotty, and the schools were struggling. Some areas were seeing problems with drugs and gangs, and some homeowners had started to move out to the suburbs. But these areas were hanging in, still functioning neighborhoods with significant social and environmental assets.

By 2015, St. Louis as a city was showing strong signs of revival. The city’s historic population loss had slowed down, although not reversed; jobs and family incomes were growing solidly if not spectacularly, and a cluster of neighborhoods in the city’s Southside were improving, perhaps even gentrifying. But the Northside middle neighborhoods were in free fall. Comparing 2000 and 2015 for these 18 census tracts as a whole:

- Their population had dropped by 22 percent

- The number of people with jobs had dropped by 25 percent

- The number of homeowners had dropped by 3,600 or 29 percent, and the homeownership rate from 59 to 50 percent.

- The median household income, adjusted for inflation, had dropped by 30 percent. Almost one out of three 2015 residents was below the poverty level, compared to less than one in four in 2000.

- The number of “other vacant” housing units, a Census measure that’s a rough proxy for abandoned units, had doubled, and was over 5,000 units.

After three decades of relative stability, all but a handful of Northside’s middle neighborhoods were turning into areas of concentrated poverty and disinvestment. This wasn’t just happening in St. Louis; the story in other cities I’ve looked at, like Chicago, Cleveland and Baltimore, was much the same.

What Happened is (and isn’t) Complicated

It’s important to start by recognizing that in 2000 these neighborhoods were already highly vulnerable to forces that would place more stress on them. In addition to the problems mentioned earlier, the first wave of homebuyers from the ’60s and ’70s was getting older, and starting to pass or move on. But it was two new things that fueled the collapse. The first is the continuing fallout from subprime lending, the housing bubble, and the foreclosure crisis. The second is a dramatic shift in the choices of African-American homebuyers. Let’s take a look at each.

If many of these neighborhoods were showing strain before the foreclosure crisis, it was the wave of subprime lending and the market collapse that followed that sent many of them over the edge. It is well known that subprime lenders targeted communities of color, starting in the 1990s by peddling cash-out refinancing deals to struggling older homeowners, and then shifting to offering high-risk mortgages to would-be homebuyers. While many were families with poor credit who had little chance of getting a conventional mortgage, many others were steered into subprime mortgages—disastrous for them but lucrative for the lenders—even though they might well have qualified for safer prime mortgages. A lot of both subprime refinancing and subprime mortgage loans were in Black middle neighborhoods. Between 2004 and 2006, 69 percent of all the home purchase mortgages made in Baden and 70 percent in O’Fallon were high-cost or subprime loans.

Baden neighborhood, St. Louis. Photo credit: Paul Sableman via flickr, CC BY 2.0

That story has been told often, but we all need to be reminded of it from time to time. What it meant, though, is that when the bubble burst in 2006 and 2007, both long-time homeowners and new ones in these neighborhoods were up to their metaphorical eyeballs in risky, unsustainable debt. The neighborhoods crashed. Foreclosures spiked, and prices collapsed.

In Detroit, house prices fell by 80 percent from 2007 to 2009. The number of new homebuyers plummeted. Most of the new buyers were investors, often people looking to make a killing in three or four years by milking the properties, cutting back on maintenance and repairs, and sometimes not even paying property taxes, knowing that by the time the city or county came after them, they’d have already made their profit, and could afford to walk away from the property. Abandoned and neglected houses started to show up on formerly manicured blocks.

After a few years, the housing market began to recover in most of the country. Overall, house prices today are higher, although not by much, than they were at the peak of the bubble in 2006. Even in Las Vegas, where prices fell by 60 percent, where virtually every homeowner was underwater and foreclosure rates were the highest in the U.S., house prices have come back, and have regained nearly three-quarters of what they lost after the bubble burst.

But not in Black middle neighborhoods, which never saw much of a bubble, and where house prices were never that high. Once they fell, with rare exceptions, they’ve stayed at or near the bottom. In O’Fallon, one of St. Louis’ most attractive historic neighborhoods, the median house price peaked in 2005 at $65,000. In 2017 it was $23,000, only one-third as much. In Chicago, where house prices are overall much higher than in St. Louis, median prices in Chatham, a still-strong Black middle neighborhood, went from $201,000 to $81,000, a 60 percent drop, over the same period.

This is the single biggest reason for the drop in Black household wealth that took place after the foreclosure crisis and the Great Recession. In one of the 18 census tracts that make up St. Louis’ one-time Black middle neighborhoods, I calculated that the loss in homeowner equity from 2008 to 2016 added up to $35,000,000; extrapolating that to the larger area, I estimate that homeowners in Black middle neighborhoods in St. Louis alone lost a total of $300 million in equity over that period.

Why have prices not come back in these neighborhoods, when they have in so many other places? It’s not that African-American families aren’t buying houses. In fact, Black homebuyers are coming back to the housing market. Mortgages to Black homebuyers, after dropping from around 400,000 in 2006—a number inflated by the volume of subprime lending—to about 100,000 in 2011, have been coming back, with 224,000 in 2016, the highest number since 2007. The difference is where Black homebuyers are buying.

Black Home Buying Is Coming Back—But Where?

In 2007, Black homebuyers obtained 801 mortgages to buy homes in the city of St. Louis. Of those, 541, or two-thirds, were for homes in predominately (80 percent or more) African-American neighborhoods, mostly the middle neighborhoods I’m talking about. A rule of thumb is that about 6 to 8 percent of homeowners move, or pass away, on average in a year, meaning that the number of new Black homebuyers was large enough to replace most, if perhaps not quite all, of the homeowners who probably moved or passed away that year.

Ten years later, in 2017, Black homebuyers obtained 281 mortgages in St. Louis. But only 84, or less than one-third, were in predominately African-American neighborhoods. What that means is first, there are far fewer homebuyers than there are houses available. And second, that the number of new homebuyers isn’t enough to replace more than a small fraction of the number of former owners moving or passing away. That, in turn means three things, which are all bad for the neighborhood. First, because the supply is so much more than the demand, prices stay at rock-bottom levels. Second, if a house sells at all, it is likely to sell to an investor, not a homebuyer, further depressing prices. Third, some houses, usually the ones that need the most work, don’t sell at all, and often end up being abandoned by their owners.

If Black homebuyers are no longer buying in these neighborhoods, are white buyers? After all, there’s been some talk that white homebuyers are becoming more open to buying in Black neighborhoods; in fact, not long ago, the New York Times even ran a story pushing that narrative. Well, yes and no. It’s true in a few gentrifying areas, mainly in the handful of cities, like Washington, D.C., or Raleigh, North Carolina, where the only “gentrifiable” neighborhoods tend to be Black neighborhoods.

But it’s very misleading, because it’s not true for the vast majority of Black neighborhoods, which are not gentrifying. If anything, the trend may be in the opposite direction. In 2007, 59 out of 3,300 white buyers got mortgages to buy houses north of the Delmar Divide in St. Louis (this is not much, about 2 percent). In 2016, the number of mortgages to white buyers citywide went down to 2,500, but the number of mortgages to white buyers north of Delmar dropped to 15, less than 1 percent of the total. There’s a fair amount of evidence that white buyers may be more open to living and buying houses in racially mixed neighborhoods—a significant share of white buyers in St. Louis did just that—but not in neighborhoods where 80 percent or more of the population is African-American.

St. Louis is not unique. In the Cleveland area, the number of mortgages for Black homebuyers in Cleveland dropped from 2007 to 2017 from 723 to 139, and in predominately African-American neighborhoods from 430 to 75. During the same period, the number of mortgages to Black homebuyers in Detroit dropped from over 4,000 to less than 500. In fact, from 2010 to 2015, more African-American families bought homes in suburban Southfield, a city with one-tenth the population of Detroit, than in Detroit. Barely one out of ten Black homebuyers in the Detroit metro bought their home in the city of Detroit.

It’s impossible to think about this without having to grapple with two inconsistent, even conflicting propositions. On the one hand, one can argue that Black homebuyers are making sound, rational decisions for themselves and their families. Almost every metro in the United States—outside hot coastal markets like San Francisco or Washington, D.C.—has a variety of suburbs where homes are affordable to a middle income family, earning around $45,000 to $75,000. Many of those suburbs offer (or at least appear to offer) distinct advantages over central city neighborhoods in terms of safety, schools, and public services. For many young Black homebuyers, suburbs may be becoming the default option. I was reminded of this when a young, newly married Black friend in Baltimore told me that they were planning to buy a home. “What neighborhood are you thinking of,” I asked innocently. “Neighborhood?” she replied, “we’re buying in Owings Mills!” (a prosperous, largely African-American suburb.)

By moving to a suburb or a racially mixed urban neighborhood, a Black homebuyer dramatically increases the odds that their property will appreciate. We don’t talk about it much, but it is well known that homeowners in middle-class Black neighborhoods pay what could be called a “discrimination tax,” in the form of lower house values and less appreciation, particularly since the foreclosure crisis. In fact, a recent study by Dan Immergluck and his colleagues at Georgia State found that homes bought by Black families since 2012 have appreciated more than those bought by white homebuyers, an amazing reversal of historic patterns.

Should We Just Move on?

What does this mean for the future of urban Black middle class or working class neighborhoods in cities like St. Louis, Chicago, or Detroit? Places like Crary-St. Mary’s, or O’Fallon, or Overbrook? Some might argue, of course, that these neighborhoods, like many immigrant neighborhoods of the 1920s, have fulfilled their function, and it’s time to move on. People are voting with their feet, that argument goes, and in the end the market will figure out whether they still have a role to play in the 21st century.

I have a lot of trouble with that argument, though, because I don’t feel neighborhoods are disposable, over and above the lives and prospects of thousands of families—including large numbers of elderly homeowners—who are seeing not only their wealth, but their quality of life, disappear. These neighborhoods have not only a physical fabric that is itself an asset, but an economic and social fabric worth saving.

As Nedra Sims Fears, the dynamic leader of the Greater Chatham Initiative in Chicago, describes her neighborhood, “a strong community that has a robust African-American culture in the very best sense of that word—cooperative, supportive, loving and nurturing.” All of this is worth fighting for, as Nedra adds, “I want folks to come back to that nurturing, supportive African-American community . . . where people can see the absolute best of what an African-American community is and can continue to be.”

Good article Alan, as usual. As we’ve discussed very briefly in passing, I do disagree a tad with the notion in the sentence “It’s true in a few gentrifying areas, mainly in the handful of cities, like Washington D.C. or Raleigh, North Carolina, where the only ‘gentrifiable’ neighborhoods tend to be Black neighborhoods.” I believe (some to many, depending on your measure of gentrification!) Black neighborhoods in quite a few cities have seen gentrification, especially in recent years. I agree that in weaker markets where segregation has been the most intense, gentrification is less common. But I would include — at least — Nashville, Atlanta, New Orleans and Oakland (to Raleigh and Washington DC) as the most obvious places where substantial gentrification has occurred in Black neighborhoods.

Also, thanks for linking to our paper! One thing I should point out in it is that we find that in metros with medium or high appreciation rates (not like St. Louis), we find that majority Black tracts and higher-poverty tracts (controlling for other characteristics) saw higher appreciation rates than predominantly white and lower-poverty tracts from 2012 to 2017. In low-appreciation metros, like St. Louis, we found no difference by race, but did find that higher income and lower poverty rates were associated with higher appreciation rates. All of this is to say that metropolitan context is critical here, and that the neighborhood dynamics of home price appreciation are very dependent on metropolitan housing market strength.

FYI every latino I know (latino is already plural and engendered) find the use of “Latinx” DEEPLY offensive. My wife, if you used that term in front of her would literally punch you and knock you to the ground, and then tell you off in rapid fire Spanish why it’s offensive, why Spanish is already perfect, why it doesn’t need de-gendering because like all Romance languages are inherently gendered and there’s nothing wrong with that. All the while she’d be kicking you and hurling obscenities at you between her explanation. Advice: never fuck with a Mexican woman! And don’t insult and appropriate her culture by using the term Latinx!