Let’s raise the standard deduction and lower tax rates to give everyone a tax cut!

Let’s raise the standard deduction and lower tax rates to give everyone a tax cut!

It should not surprise you that since this is a description of the House GOP tax plan that it’s not as good as it sounds.

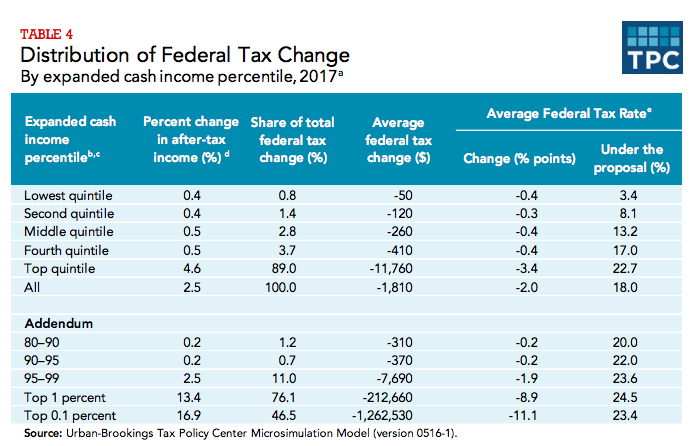

Indeed, an analysis from the non-partisan Tax Policy Center shows that, surprise, surprise, the benefits would be extremely concentrated among the wealthy, who would save tens of thousands to millions every year, compared to $50 to $410 for the lower four-fifths of the income scale. That’s a 4.6 to 16.9 percent increase in after-tax income, depending if you are merely well off or super-rich, while everyone in the bottom four-fifths sees, at most, a 0.5 percent increase. (See table.)

Of course the effects would be worse than that sounds. Given that that analysis also shows modest and short-term GDP growth resulting from these tax cuts that would be dwarfed by the loss of revenue in the trillions, this plan would almost certainly mean dramatic scale back or cancellation of dozens of ways we currently take care of the vulnerable or those going through economic dislocation.

Of course the effects would be worse than that sounds. Given that that analysis also shows modest and short-term GDP growth resulting from these tax cuts that would be dwarfed by the loss of revenue in the trillions, this plan would almost certainly mean dramatic scale back or cancellation of dozens of ways we currently take care of the vulnerable or those going through economic dislocation.

The downsides of losing affordable healthcare and housing support, veteran benefits, food stamps, unemployment benefits, defense against employer abuses, publicly created jobs, and the like would exponentially outstrip $50 to $410 per year in additional income.

But wait, there’s more.

Raising the standard deduction is at least in itself a move that does not mostly support the wealthiest, who would still likely save more by itemizing their deductions.

However, Jordan Weissman over at Slate has pointed out that some middle-income homeowners who would see a small income gain with the deduction change might well experience a significantly greater loss of assets at the same time. How?

With a higher standard deduction, far fewer homeowners are going to get any benefit from the mortgage interest deduction. And this, say economists, is likely to reduce the value of their homes because the mortgage interest deduction artificially inflates home prices because of the expectation of being able to deduct the interest.

This is a prediction that will be extremely variable by housing market, and would take a while to have practical implications for many owners who don’t draw on their home equity for day to day living and who can’t log on somewhere and watch their official home value fall, so it might be hard for homeowners to register it immediately as a concrete loss against a slightly smaller tax bill, despite Weissman’s energetic efforts to sound the alarm. But for some of them at least it could certainly matter.

And the implications apparently bother the homebuilding industry so much they are going into full-scale war mode about it:

“We’re looking at the current draft plan as an assault,” NAHB [National Association of Home Builders] Chief Executive Officer Jerry Howard said. “By raising the standard deduction you put money in people’s pockets, yes, but you’re not encouraging them how to use the money.”

Heaven forbid that we don’t tell people how to use their money …

What the NAHB is missing, of course, is that the problem is not raising the standard deduction. It’s not even the idea that the country might eventually stop subsidizing homeownership. The problem is leaving the mortgage interest deduction as a boon to the wealthy financing luxury homes while abruptly cutting off its relevance for everyone else.

That effectively takes a tax provision that was already badly tilted toward favoring the wealthy and makes it exclusively available to them. This is an unconscionable increase in inequity, the opposite of turning the tax code right side up.

Making the sorts of progressive reforms to the mortgage interest deduction that have long been talked about—primarily capping it and making it a refundable credit you don’t need to itemize for—would solve this part of the problem.

Too bad it wouldn’t fix the underlying disaster of bankrupting the government in order to give tax breaks to the wealthy.

Image: Courtesy of Pam Lane, via flickr, CC BY-NC-ND 2.0

Comments