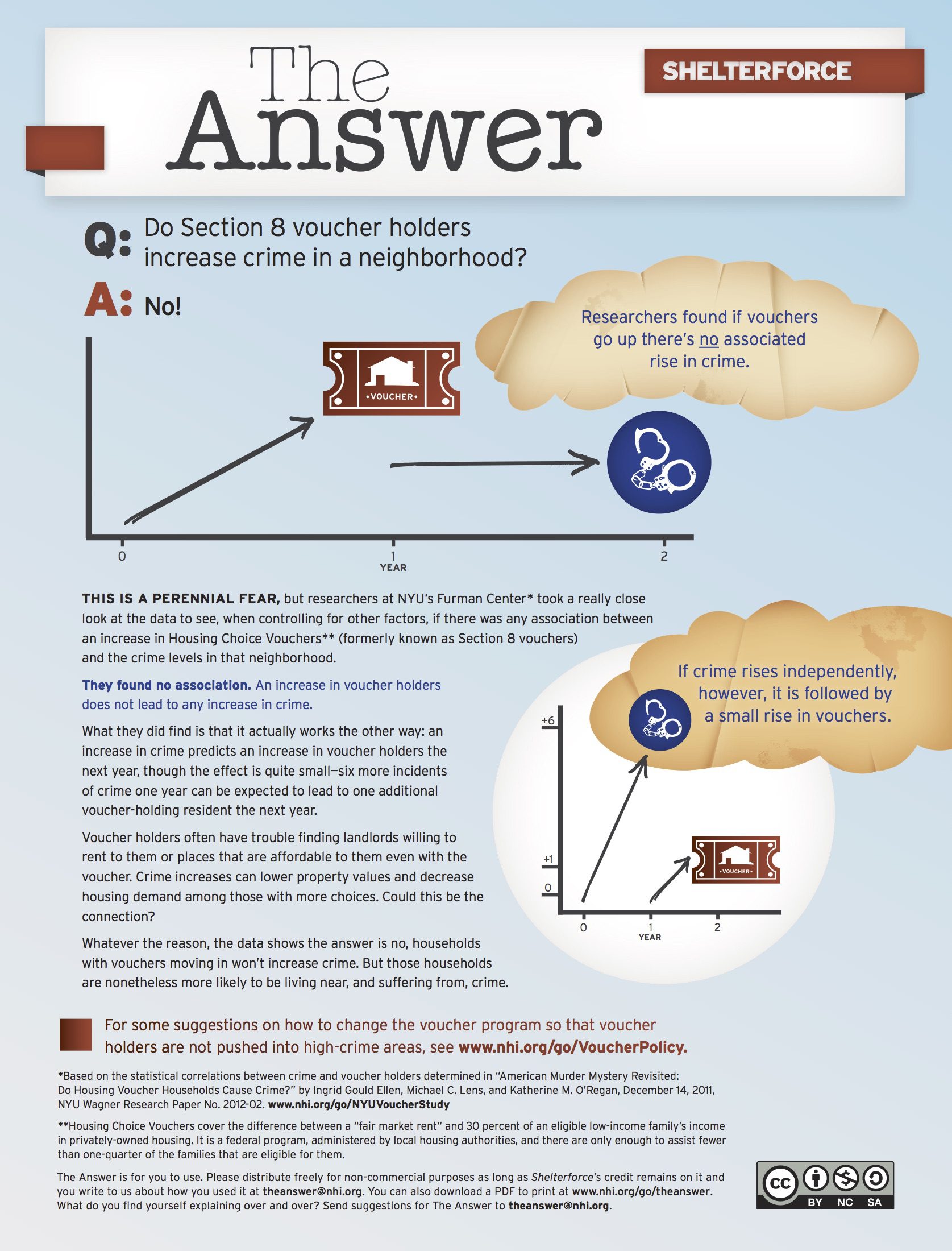

Brett and Isis Henderson jump for joy outside their new home, made possible by a community land trust and a VA-backed mortgage. Photo by Tiffany Hunter

Brett Henderson has been an Army veteran for over 17 years. He grew up in Ohio and moved back from Los Angeles with his wife, Isis, when they married. They fell in love with the eclectic, artsy community of Yellow Springs, home of Antioch College, where they rented a small two-bedroom apartment while looking for a house in which to raise their future family.

Property values in Yellow Springs were significantly higher than those in most other Ohio towns, but they still found a dream home: an affordable, new construction, highly energy-efficient starter home, offered by local housing nonprofit Yellow Springs Home, Inc. through the community land trust (CLT) homeownership model.

If Henderson could get a Dept. of Veterans Affairs guaranteed mortgage, with its low to no downpayment requirement, they would be able to buy this home.

But to make it work, Yellow Springs Home first had to get the regional VA office to be officially willing to guarantee a loan for a community land trust purchase, something many lenders are unfamiliar with and wary of.

VA Loans and CLTs: A Match

In the CLT model, the land trust sells the house, but keeps ownership of the land, giving owners a 99-year ground lease. It works by lowering the base price of a home to an affordable level through a one-time subsidy. In return, if selling, the homeowner must sell to another underserved buyer for a reduced price, paying forward some of the help they received while earning a return on their investment. The CLT model is designed not only to provide homeownership opportunities to low- to moderate-income households, but also to keep the homes affordable for succeeding generations of buyers. Much of the subsidy stays with the home, stretching its impact while also creating wealth.

The CLT goal of extending sustainable homeownership to more households aligns with the goals of VA loans. The Hendersons are part of a new generation to qualify for a range of housing benefits through the VA’s Home Loan Guaranty Program, which has helped service members, veterans, and eligible surviving spouses become and remain homeowners since 1944.

VA loans have competitive interest rates, and often don’t require any downpayment. In 2013 alone, nearly 630,000 loans were guaranteed by the VA. More than 200,000 of those did not have a downpayment.

A one-time funding fee rolled into the loan acts in lieu of private mortgage insurance, further reducing monthly payments. To be eligible, a veteran household must have a good credit score, sufficient income, meet certain service requirements, and have a valid Certificate of Eligibility. The products work with a variety of private lenders and mortgages, including CLT mortgages.

The VA program and CLTs also align well in their concern for the long-term success of their borrowers. VA loans come with post-purchase services to prevent foreclosure—the VA oversees mortgage loan servicers to ensure that they offer options for home retention and alternatives to foreclosure. CLTs use their ongoing relationship with the owners as an opportunity to exercise stewardship through a range of in-depth pre- and post-purchase support services to promote successful homeownership and prevent foreclosure. Nationally, CLT homeowners are far less likely to return to renting or to go through foreclosure than market-rate homeowners.

Despite this alignment, not all VA regional offices are familiar with land trusts, so CLTs wanting to help veterans buy their homes using the VA program may have some legwork to do.

Creating a VA and CLT Partnership

Yellow Springs Home, Inc. is a CLT operating out of southwest Ohio in close proximity to Wright Patterson Air Force Base, the largest single employer in the state, with more than 26,000 employees. The land trust was developed in the mid-1990s at the recommendation of a housing task force formed by city council, after passionate local citizens expressed concern about skyrocketing housing prices. Its mission is to strengthen community and diversity in Yellow Springs and Miami Township by providing permanently affordable and sustainable housing.

When the Hendersons came to Yellow Springs Home, Brett had been pre-approved for a VA-backed mortgage. A handful of CLTs around the country already work with the VA-backed mortgage, but since this was the first CLT to approach this regional office, national and regional approval of the CLT’s ground lease was required.

This three-month process included contacting VA jurisdictional headquarters in Cleveland, Ohio, and sending documentation, including an overview of the CLT homeownership model, the model ground lease in use, an approval letter from another jurisdiction, and a letter from the homebuyers, Brett and Isis.

The primary concerns on the VA’s part were some restrictions found in the ground lease regarding who can purchase the home if it is sold—for a certain duration of time, the homeowner must sell to another low- to moderate-income household at a price determined by a resale formula. CLTs often assist in identifying the next buyer, and this restriction is at the heart of encouraging place-based affordable housing for generations. There are also stipulations about who the ground lease can be assigned to, including children, partners, spouses, and other members of the household. These provisions may be seen as in conflict with VA guidelines that discourage restrictions on mortgage transferability and assignability.

While the ultimate decision may vary from region to region, it seems the restrictions that CLTs use may be found either within the guidelines, or worthy of an exception to them, by a VA office if some combination of the following are satisfied:

- the CLT can show that the restrictions do not materially affect the reasonable value of the subject property;

- the veteran provides a written and signed statement that they are fully informed of the restrictions (Generally in place, since the model CLT ground lease includes letters of stipulation and acknowledgement, which require the homebuyer to review the contract with an attorney prior to closing.);

- the CLT can show its ground lease is used commonly in its service area; and

- the CLT can show the provisions sufficiently protect the homeowner and government.

The fact that a veteran buying a CLT home is by definition going through a program designed to assist low- and moderate-income purchasers also appears to weigh in land trusts’ favor in applying for an exception to the guidelines—it was listed as a factor in Yellow Springs Home’s approval letter.

For CLTs looking to work with VA loans, it may help to refer concerned parties to Fannie Mae, which has an official set of practices for working with mortgages for CLT properties and for valuing the leasehold estates. The National CLT Network is also developing tools and model documents about accessing the VA housing program.

[RELATED ARTICLE: Understanding Community Land Trusts]

Once a decision is made at the regional level it is sent to the national office for final approval. The end result of the VA approval process is a letter approving a blank, unsigned ground lease that a CLT can use to assure mortgage lenders and underwriters.

The result of Yellow Springs Home getting that letter is that today, Brett and Isis are the proud owners of an affordable three-bedroom, two-bath home with a HERS rating of 57—meaning it uses less than half the energy of a conventional home. They couldn’t be happier. It aligns with their personal goals of energy efficiency (Brett works for a solar company) and they feel right at home. “It’s a dream come true,” Isis says.

According to Brett, “We are very grateful for Yellow Springs Home, Inc.’s willingness to take on this challenge. They could have said, sorry, the VA-backed mortgage isn’t an option with our program, but instead they chose to roll up their sleeves with us and figure out how to make it happen, and happen it did. The VA-backed mortgage empowered us to act fast on our ideal home.”

Comments